{kind=link}

Are you aware, kind of, how RSUs work, however ESPPs are a whole thriller? Be part of lots of our purchasers in that confusion. And admittedly they’re stupidly sophisticated for the amount of cash they’re price to you.

And whereas Worker Inventory Buy Plans are pretty widespread in massive public tech corporations, they’re not practically as widespread as RSUs. Google and Amazon, for instance, have RSUs however not ESPPs.

[Note: This article was originally written in 2016. I went to send it to a client and was hahrified, HAHRIFIED, by what I found. So I almost entirely rewrote it. You ever read something that you wrote 7 years ago? Yeah…]

Because it seems, ESPPs could be Free Cash. Properly, there’s some threat, and my compliance guide might be having an aneurysm over using that phrase, however typically you may maintain the danger actually low and are available out…perhaps just a few thousand {dollars} forward.

I hope this text helps you perceive how they work…and likewise the way you in all probability shouldn’t get too excited over them.

[Note: This article is about qualified Employee Stock Purchase Plans (as opposed to non-qualified). The qualified kind is most likely what you’ll receive as an employee of a tech company.]

How Does an ESPP Work?

I can simply clarify at a really excessive stage the way it works:

An ESPP lets you purchase firm inventory at a reduction (as much as 15%) off the inventory worth.

First, Some Phrases You Have to Perceive

Something extra detailed than that, you’re gonna need to endure some vocabulary classes first:

- Providing Interval: That is often one to 2 years lengthy. An important factor for you, the worker, that comes out of the Providing Interval is the worth of the inventory firstly of the Providing Interval. This shall come up later!

- Buy Interval: There are often a number of Buy Intervals inside an Providing Interval. A standard setup is to have a one-year Providing Interval, with two 6-month Buy Intervals inside it. Or a two-year Providing Interval, with, you guessed it, 4 6-month Buy Intervals inside it.

Your participation within the ESPP is taken Buy Interval by Buy Interval. Even when the Providing Interval is 2 years lengthy, you may select to take part in just one Buy Interval.

- Lookback: With a lookback, that (15%?) low cost is calculated off the decrease of two costs: the inventory worth on the starting of the Providing Interval, and the inventory worth on the finish of the present Buy Interval). If your organization inventory has gained loads of worth for the reason that starting of the Providing Interval, you may maybe see how good this may be!

Lookbacks are good! And fairly widespread in Huge Tech. With out a lookback, the low cost is taken off the worth on the finish of the present Buy Interval. That is simply advantageous, however it’s by no means going to offer you an opportunity to make some huge cash.

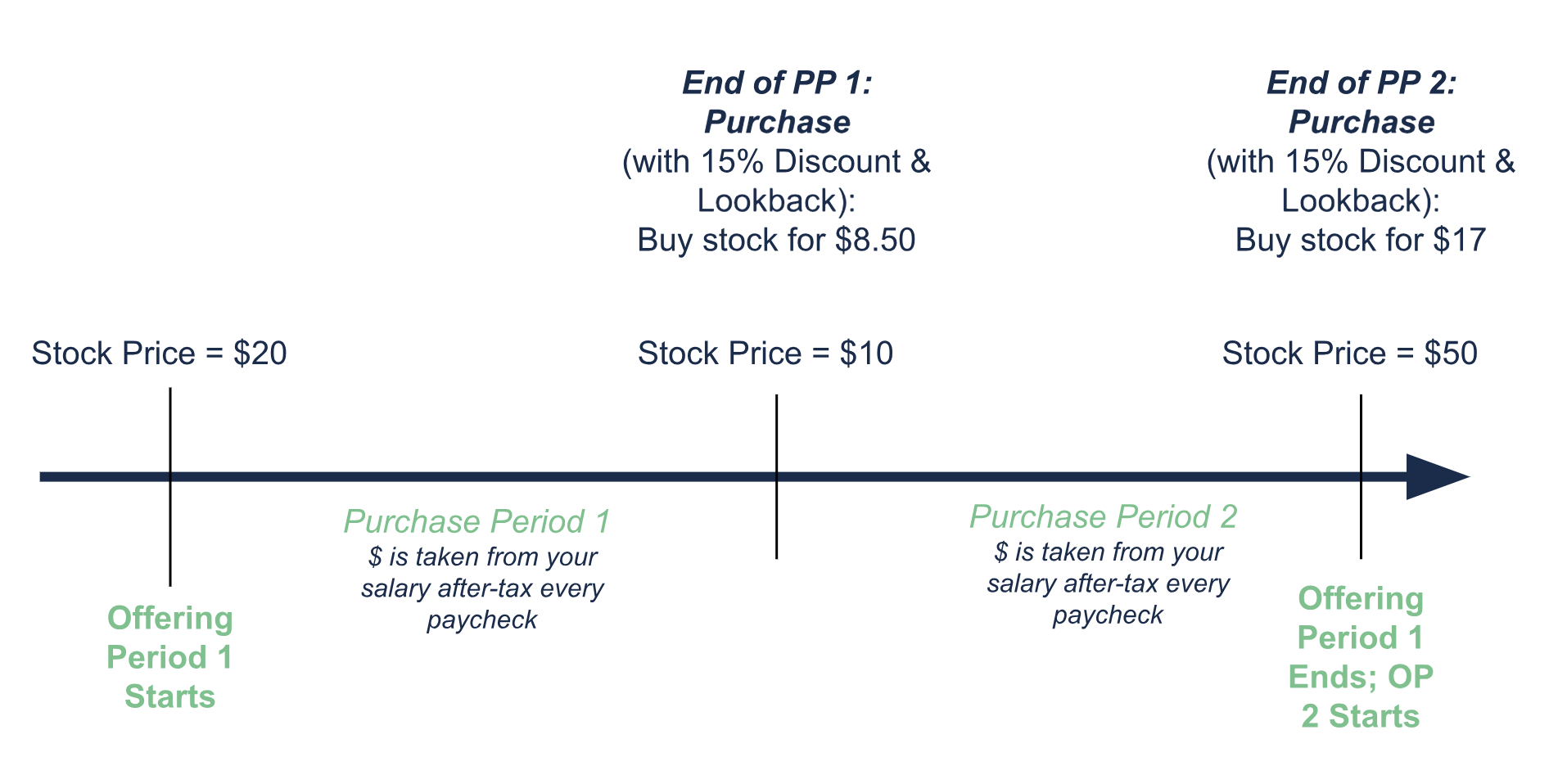

Airbnb’s ESPP is the very best instance I’ve:

- It listed at $68 when it IPOed. Its ESPP Providing Interval began that day, providing the best low cost (15%) and a lookback.

- When its first Buy Interval ended 6 months later, the worth was nearer to $150.

- Airbnb workers collaborating within the ESPP received to purchase ABNB inventory at 15% off $68 = $57.80!

- In conclusion: Whoa.

Now, the Precise Course of

- Select the share of your wage to deduct out of your paycheck. That is set anew for every Buy Interval.

- Your organization caps the share you may contribute; a typical restrict is 10%.

- You may, in reality, solely purchase $25,000 price of firm inventory annually (that $25,000 is calculated based mostly on the inventory worth firstly of the Providing Interval). Usually, which means you’re fairly restricted in how a lot you should purchase.

- That cash is withheld from every paycheck for the whole Buy Interval.

- To provide you a way of scale, if you happen to max out your participation within the ESPP over the course of a yr, you’re going to have about $1770 much less coming house to you per thirty days in your paycheck. (That’s $25,000 minus the standard 15% low cost, divided by 12 months.)

- This cash is after tax cash. You don’t get a tax profit by setting it apart, as you’ll for contributing to a pre-tax 401(okay).

- It will get stored as money for that complete Buy Interval and isn’t in danger.

- If at any level throughout the Buy Interval, you want that money, you may ask for it again. You may get it again…however if you happen to do, you may’t reenroll within the ESPP till the following Providing Interval begins. It’s a pleasant failsafe, although.

- Firm inventory is bought with that gathered cash on the finish of the Buy Interval.

- The inventory is bought on the low cost to the inventory worth.

- In case your plan has no lookback, that low cost is utilized to the worth now. If there’s a lookback, then you definitely use the cheaper price of now or earlier (as defined above).

- You now personal some shares of your organization’s inventory in a taxable brokerage account of your employer’s selection (Constancy, Schwab, and so forth.).

- This is similar account that your RSU shares would additionally present up in when your RSUs vest (if you happen to additionally get RSUs).

Ought to You Take part?

Most likely.

Needless to say some ESPPs suck. My husband had an ESPP at HP a few years in the past. They supplied a 5% low cost. I bear in mind calculating that we might earn $400 after-tax over a complete yr of participation. I made a decision it wasn’t definitely worth the problem.

Is there a small low cost? Is there no lookback? My opinion of your participation is extra alongside the strains of “meh.”

However when you’ve got a 15% and a lookback? These are some reeeeeal good phrases…

Estimate How A lot Cash You Can Get From Taking part

Earlier than you resolve to or not, it’s essential to know:

- Low cost

- Whether or not there’s a lookback

- Max quantity you may contribute

Then run (or relatively, approximate) the numbers in your firm’s ESPP:

- Multiply $25,000 by the low cost, let’s say 10% = $2500.

- That is the quantity of pre-tax earnings you’ll obtain, assuming you don’t have a lookback. If in case you have a lookback, then you definitely actually can’t know the way a lot this shall be price to you.

- Estimate your complete federal and state tax charge, let’s say 35% federal + 9% state + 0.9% Medicare = 44.9%.

- Subtract that tax quantity off your pre-tax earnings from the ESPP: $3750 – 44.9% = $1377.

- That is the amount of cash you’ll really usefully make from the ESPP.

Any time you’re coping with inventory compensation, it’s essential to assume alongside three strains:

- Taxes

- Your funding portfolio

- Normal planning

Know How It Impacts Your Taxes.

When the inventory is bought for you on the finish of the Buy Interval, you don’t owe any taxes. The taxes come into play whenever you promote the inventory.

(By the best way, the tax remedy of ESPPs can get fairly bushy, “qualifying disposition” and “disqualifying disposition” and all that. I paint solely a basic image of issues right here, with the aim of not hurting your mind. For those who’re going to truly take part in an ESPP, you’ll profit from some Detailed Tax Evaluation.)

For those who promote as quickly as potential after acquisition (typically there’s a few-day wait earlier than the buying and selling window opens): You’ll pay unusual earnings tax—the identical tax charge you pay in your wage—on the discounted quantity and certain little else in tax as a result of the inventory received’t change a lot in worth.

For those who promote inside a yr after acquisition or inside two years after the beginning of the related Providing Interval): It is best to pay the identical unusual earnings tax on the low cost quantity, however as well as you pay short-term capital features taxes on any subsequent features.

For those who wait at the least one yr after acquisition and two years after the beginning of the related Providing Interval to promote: Once more, you’ll pay unusual earnings tax on the low cost quantity, and this time you pay long-term capital features taxes on any subsequent features. If the inventory has fallen in worth because you acquired it, it’s potential you’ll not owe any tax in any respect.

Lengthy-term capital features tax charges are decrease than short-term capital features tax charges, that are the identical as unusual earnings tax charges. It will get extra sophisticated from there, and this isn’t a tax weblog put up, so I’ll depart you with “Use a CPA who is aware of fairness comp.”

For those who actually need to see a numbers-heavy instance of how taxes on an ESPP would possibly work, take a look at what TurboTax has to say about it. Don’t say I didn’t warn you.

Don’t Let Firm Inventory Dominate Your Portfolio.

Or at the least, be very conscious if you’re, and what the dangers are of doing that.

The query now’s: How a lot of the corporate inventory ought to I maintain?

It’s straightforward to construct up a big holding if you happen to’ve labored for a similar firm for years and also you’ve been frequently buying inventory this fashion and that (often by way of RSU vests and ESPP purchases).

Though I often desire to carry no particular person inventory, you would in all probability persuade me that 5% of your funding portfolio is an inexpensive higher restrict. Particularly in case your persuasion technique includes Rechuitti truffles.

The most secure approach to maximize your worth from the ESPP is:

Contribute as a lot as you may to the ESPP, and promote all of the inventory as quickly as potential after receiving it.

Simply as you need a diversified portfolio, you need a diversified monetary image, too. It will increase your complete monetary threat to have each your investments and your job with the identical firm. Certainly 2022 and 2023 have proven us painfully simply how dangerous employment and inventory worth can get within the tech trade. Yowch.

Know How It’ll Have an effect on Your Money Move and Financial savings.

I feel ESPPs are, to first order, a cash-flow problem.

ESPPs are enforced financial savings.

ESPPs often don’t present a lot in the best way of additional after-tax {dollars}. For those who purchase $25,000 price of inventory at a 15% low cost, that’s $3750 of “free cash,” which is then topic to unusual earnings taxes of let’s say 45% federal + state, leaving you with $2062 of after-tax cash.

However! what you really get on the finish of a 6 month buy interval is not only that “free cash.” It’s all of the inventory you bought, which is price much more. Now, most of that worth might be your money that went into shopping for that inventory, however hear me out:

That is enforced financial savings. Sort of like paying an excessive amount of in your taxes and getting a tax refund!

And, for the document, I luuuurve these sorts of behavioral hacks.

What is going to you do with the additional cash on the finish of the Buy Interval?

What is going to you do with the cash on the finish of the Buy Intervals? (Let’s assume you promote the shares.)

Are you saving up a home downpayment, or in your child’s faculty?

Do you have got a debt you’d actually prefer to repay, like a mortgage or pupil mortgage?

This might be a possibility to make some gratifying, prompt monetary progress.

You Should Reside on Much less Earnings 6 Months at a Time.

Once you take part within the ESPP, your paycheck goes to be decrease than you’re accustomed to, as a result of the employer is withholding cash for the eventual inventory buy. Are you able to survive on that smaller paycheck?

If not, what is going to you employ to pay your payments? Do you have already got a stash of money you may deplete? Or can you employ your RSU earnings (or the proceeds from the earlier Buy Interval’s ESPP gross sales) to pay your payments now?

Miscellaneous however Probably Helpful Bits about ESPPs

- You understand how it’s all tax optimize-y to donate appreciated shares of inventory as a substitute of money to charity? (Now you do.) ESPP shares are not good examples of this, due to the built-in little bit of unusual earnings from that “low cost” cash. Donate one thing else.

- Let’s say you allow your job with the ESPP. You could have shares from each RSUs and the ESPP. You need to switch these shares to a different brokerage account some other place. Almost definitely you’ll be capable to switch the shares from RSUs however not from the ESPP.

Why? As a result of whenever you ultimately promote the ESPP shares, even if you happen to now not work on the firm, you’ll owe unusual earnings tax on the low cost quantity, and that unusual earnings will run by way of your organization’s payroll division. Which suggests they should maintain observe of it.

So, there we go.

More often than not, ESPPs are “Yeah, certain, go forward and take part. Simply promote the inventory instantly to scale back your funding threat. Ensure you know the way you’re going to pay your payments whereas your paycheck is decreased for the following 6 months. And let’s make a plan for the cash you’re gonna have when you promote.”

Typically they’re “Lord, this isn’t definitely worth the effort.”

And barely they repay massive time, often within the occasion of an ESPP that begins at IPO date, and the IPO goes rather well. However actually, it’s at any time when there’s a lookback and the inventory worth rises loads throughout the Buy Interval.

Go forth and “meh”!

Are you questioning if or how you must take part in your organization’s Worker Inventory Buy Plan? Are you attempting to determine how one can make it work with the remainder of your funds? Attain out and schedule a free session or ship us an e mail.

Join Move’s twice-monthly weblog e mail to remain on high of our weblog posts and movies.

Disclaimer: This text is supplied for academic, basic data, and illustration functions solely. Nothing contained within the materials constitutes tax recommendation, a suggestion for buy or sale of any safety, or funding advisory companies. We encourage you to seek the advice of a monetary planner, accountant, and/or authorized counsel for recommendation particular to your state of affairs. Copy of this materials is prohibited with out written permission from Move Monetary Planning, LLC, and all rights are reserved. Learn the complete Disclaimer.