{kind=link}

Initially written for Livewire

I’ve to confess to a contact of schadenfreude watching the demise of Silicon Valley Financial institution (SVB) on Twitter this week. All of these Silicon Valley free-marketeers screaming on the authorities to rescue them? Caps lock completely on and all.

Silicon Valley Financial institution $SIVB studies earnings tomorrow

Traders have rightfully been fixated on $SIVB‘s massive publicity to the harassed enterprise world, with the inventory down loads.

Nonetheless, dig just a bit deeper, and you can see a a lot larger set of issues at $SIVB… 1/10

— Raging Capital Ventures (@RagingVentures) January 18, 2023

They’re proper, although.

Ethical hazard is a significant issue within the fashionable economic system. Bailouts and rescues have gotten ubiquitous. Not solely does that create a system of heads personal traders win, tails the taxpayer loses, it derails inventive destruction. Dumb concepts must fail. Poorly deployed capital must be redeployed to companies and managers which have the great concepts.

That’s the way you get productiveness development within the economic system. The truth that we don’t let anybody go bust as of late has been a big contributor to productiveness development declining relentlessly for the previous 20 years.

For all that, no financial institution depositor ought to ever lose their cash in a developed-world economic system. It’s absurd to suppose each single small and medium sized enterprise ought to be working round analysing financial institution steadiness sheets to find out the credit score worthiness of their deposits. In case you deposit your cash in a regulated, licenced, developed-world financial institution, you could have each proper to anticipate that your cash shall be there as and if you want it.

Regulated and capitalised

Earlier than we get onto the options, it’s price noting that loads of traders ARE dropping cash right here. SVB was listed on the inventory trade. Its $11bn of fairness has been worn out (the market capitalisation was $43bn on the peak). Unsecured lenders to the financial institution are in for a haircut too. And the taxpayer is unlikely to lose a lot, if something. There are far worse examples of ethical hazard if you wish to discover them.

But it surely was an abject regulatory failure. Take a second to learn this Tweet thread from Invoice Martin (@RagingVentures on Twitter), a hedge fund supervisor. In 10 tweets, utilizing nothing however the newest publicly obtainable steadiness sheet, Martin highlighted probably the most basic liquidity mismatch you may conjure up. How can a regulated financial institution make investments virtually all its at-call deposits in property with a period higher than ten years? How can a regulator allow them to do this? The only, most elementary liquidity guidelines ought to cease a regulated financial institution from taking such a silly danger.

Financial manipulation the basis of many issues

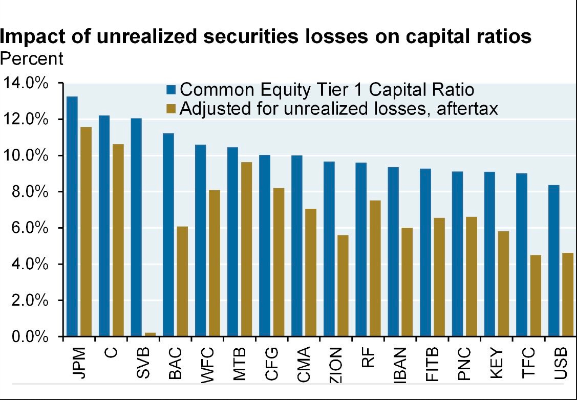

My finest guess is that this gained’t be a widespread concern within the banking sector. Not many financial institution treasurers are that silly. For many banks, together with the bigger regionals within the US, valuing their property at present rates of interest won’t considerably influence their capital place. As you possibly can see within the chart under, for SVB, revaluing its steadiness sheet to market values worn out all its Tier 1 capital.

Affect of unrealized securities losses on capital ratios. Supply:JPMAM

It’s emblematic, although, of the stupidity that may occur when rates of interest are manipulated to zero. From industrial property to unlisted infrastructure property to Australia’s housing market, attempting to rescue an economic system via ultra-low charges has penalties that are actually changing into apparent to everybody.

Financial coverage is a really blunt, typically ineffective instrument with wide-ranging unintended repercussions. But it has change into the first instrument relied upon in occasions of disaster, regardless of fiscal coverage (authorities spending) being a much more efficient technique of focused stimulation.

Central Financial institution governors shouldn’t be on the homepage of the Each day Mail. The position that optimistic actual rates of interest play in environment friendly capital allocation ought to be given extra weight. And inspiring individuals to overextend themselves at artificially low charges could cause monetary crises.

The collapse of a US regional financial institution could be a comparatively containable concern. It gained’t be the final catastrophe brought on by the financial insanity of the previous few years. If inflation dangers begin to recede and the economic system begins to weaken, I hope these classes aren’t forgotten.