{kind=link}

U.S. oil and gasoline manufacturing boomed throughout the years main as much as the pandemic. From 2011 to 2019, oil manufacturing greater than doubled and dry pure gasoline manufacturing rose by greater than half. Remarkably, these positive aspects occurred regardless of lackluster funding spending and hiring. As an alternative, increased manufacturing got here largely from productiveness positive aspects, by way of wider adoption of fracking applied sciences. Extra just lately, manufacturing recovered sluggishly from the pandemic downturn regardless of a fast restoration in costs. Our evaluation on this submit means that slower productiveness progress and buyers’ demand for increased returns have made U.S. corporations prepared to spice up output solely at a better threshold oil value.

Productiveness Drove a Growth in Oil and Fuel Output

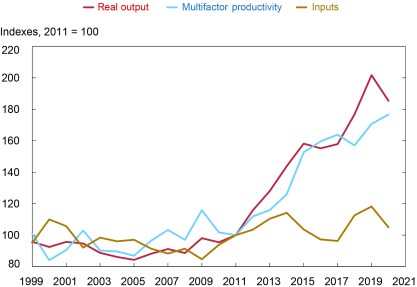

U.S. oil and gasoline manufacturing boomed throughout the years main as much as the pandemic. Actual internet output within the oil gasoline extraction trade greater than doubled from 2011 to 2019 in line with information printed by the U.S. Bureau of Labor Statistics (BLS), a growth proven by the highest line of the chart beneath. The sharp rise within the BLS index was pushed by an unlimited enhance in bodily portions. Crude oil manufacturing greater than doubled over the interval, whereas dry gasoline manufacturing rose by greater than half. This progress got here as a shock as manufacturing had stagnated over the prior twenty years.

Oil and gasoline extraction surged within the final decade

Notes: Actual output is a composite of oil and gasoline extraction, taking account of the combo and worth of particular oil and gasoline varieties. Actual inputs are comprised of capital, labor, and intermediates, aggregated utilizing manufacturing price shares. The index additionally takes into consideration the combo and worth of particular oil and gasoline product varieties.

The chart additionally reveals that the BLS measure of actual inputs rose solely modestly over the interval. As an alternative, the increase was pushed largely by productiveness positive aspects—by the effectivity with which capital, labor and intermediate inputs have been used, somewhat than by their amount. This conclusion might be quantified by way of the financial idea of multifactor productiveness (MFP)—a measure of the portion of output progress not defined by mixed progress in inputs. The instinct is that will increase in MFP mirror technological and organizational modifications that increase output for a given amount of inputs.

In response to the BLS information, actual inputs to grease and gasoline extraction grew by solely 18 p.c from 2011 to 2019 (the gold line in our chart). Multifactor productiveness, derived as a residual between output progress and enter progress, was up by barely over 70 p.c over the interval (blue line).

Extra detailed information present that enter progress got here largely from elevated use of intermediates: power, supplies and bought providers. Capital inputs rose by solely about 5 p.c over the interval, with funding spending principally going to offset depreciation. Labor inputs truly declined, reflecting a drop in hours labored.

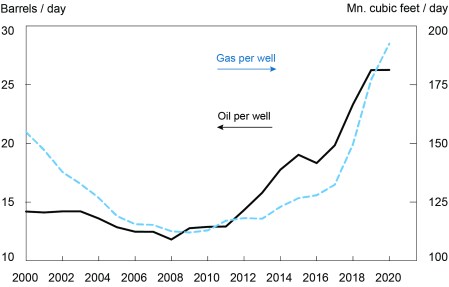

The oil and gasoline productiveness increase owed to the adoption and refinement of fracking and associated applied sciences. These applied sciences enabled producers to entry oil and gasoline embedded in shale and different “tight rock” formations and to realize exceptional positive aspects in drilling effectivity. Certainly, information from the U.S. Vitality Data Company, seen within the chart beneath, present crude oil manufacturing per lively properly greater than doubling from 2011 to 2019, and gasoline manufacturing per properly rising 50 p.c. Complete wells in operation, in the meantime, remained basically flat.

Fracking know-how drove sturdy productiveness positive aspects

Notice: The chart reveals common output per lively properly.

Sturdy Productiveness Development Didn’t Imply Increased Income

It appears pure to assume that sturdy productiveness progress would imply sturdy revenue progress. In spite of everything, corporations can enhance output with out spending extra on inputs. Occasions didn’t prove that approach.

Our estimate of financial income, proven by the blue bars within the chart beneath, declined over the interval, with persistent losses setting in after 2014. (We depend on our personal estimate as a result of the official U.S. revenue information don’t embody unincorporated companies, which maintain about half the sector’s capital inventory.) This revenue efficiency translated into subpar returns for buyers. Certainly, the Vitality Data Administration estimates that the return on fairness for power firms was persistently beneath the return for manufacturing firms all through the fracking increase.

Increased productiveness has not been mirrored in increased income

Notes: Income are equal to worth added much less labor compensation, depreciation, taxes on manufacturing internet of subsidies, and internet curiosity funds. Web curiosity funds are set equal to 65 p.c of funds by the mining trade, since information for the oil and gasoline trade will not be reported individually. Oil costs consult with WTI.

The mismatch between productiveness and monetary efficiency owes to weak costs. Oil and gasoline costs held close to all-time highs from 2011 by late 2014 however then tumbled and remained low. In 2019, oil costs (the dotted black line within the chart) averaged 40 p.c beneath their 2011 degree. Pure gasoline costs at Henry Hub averaged 35 p.c beneath their 2011 degree. These value developments assist clarify why funding and hiring have been so anemic. What productiveness progress gave, decrease costs took away.

A comparability of 2019 with the state of affairs in 2009 can also be instructive. Oil costs have been about the identical in each years. But income have been decrease in 2019, with increased enter prices placing a lid on the trade’s monetary efficiency regardless of exceptional productiveness positive aspects.

The Tepid Current Response to Increased Vitality Costs

The onset of the pandemic despatched power costs right into a tailspin and sharp cutbacks in manufacturing and exploration adopted. However costs recovered and, by March 2021, oil costs had risen to $63/barrel, above the 2019 common. Pure gasoline costs moved previous their 2019 common much more rapidly, by late 2020. Each oil and gasoline costs then continued to pattern increased.

U.S. manufacturing and funding have been sluggish to get better regardless of the bounce again in costs. Crude oil manufacturing in June 2022 was about 7 p.c beneath its degree in early 2020. Fuel manufacturing was solely barely above that degree. And actual capital expenditure within the second quarter for oil and gasoline extraction was down some 15 p.c from its pre-pandemic tempo.

Why did U.S. manufacturing and capital expenditure reply so sluggishly? We see three associated explanations—with essential implications for future oil and gasoline manufacturing.

Uncertainty. Earlier than Russia’s invasion of Ukraine, there have been believable situations below which oil costs may fall: one other pandemic-induced slowdown, easing of sanctions on Iran and Venezuela, or increased manufacturing from Saudi Arabia. On this connection, producers thought of the sizeable losses in 2015 and 2020 and have been reluctant to increase.

Investor stress. The 2022:Q1 Dallas Fed Vitality Survey requested corporations about elements holding again manufacturing. The commonest reply was investor stress to keep up excessive returns, with nearly a 60 p.c share. Current analyst discussions additionally emphasize this theme. Holding capital spending low leaves extra money to return to buyers as dividends or to pay down debt. This investor stress for “capital self-discipline” is after all linked with uncertainty. Having been burned twice within the final decade, buyers are extra actively asking for increased returns.

Slower MFP positive aspects. Corporations could also be responding to worries that the trade is nearing the tip of outsized productiveness positive aspects. On this connection, MFP progress slowed to a 2.3 p.c annual tempo over 2016-2019—nonetheless spectacular, however a pointy step down from an almost 10 p.c tempo over 2011-2016. The slowdown possible displays the maturing and now close to common adoption of fracking applied sciences.

A take a look at long-term efficiency throughout industries helps the notion that productiveness progress within the oil and gasoline sector will stay decrease than within the 2010s. Throughout successive multiyear durations, there’s a marked tendency for industries seeing particularly sturdy MFP progress throughout one interval then experiencing muted progress throughout the subsequent. A slowing within the sector’s MFP progress would sharpen the trade-off between output and capital self-discipline. Boosting output would then require increased funding outlays, leaving much less money to return to buyers.

The 2022:Q1 Dallas Fed survey additionally requested corporations what value could be wanted to push the trade into “progress mode.” Some 41 p.c of corporations mentioned $80-100/barrel could be wanted. One other 29 p.c cited a value above $100-120/barrel or increased. (The remainder mentioned the choice didn’t rely upon costs.) The stronger pickup in extraction exercise since Russia’s invasion of Ukraine, with costs staying above $100/barrel, is according to this survey response. Notably, related questions within the third quarter of 2016 and the fourth quarter of 2017 positioned progress mode at beneath $70/barrel. Briefly, U.S. corporations are apparently prepared to increase manufacturing aggressively solely at a a lot increased value threshold than within the current previous.

A shift to a better value threshold has international implications. Throughout the 2010s, U.S. corporations performed a key position in maintaining international power costs low, by way of their outsized contribution to progress in international gasoline and power manufacturing. Certainly, the Division of Vitality estimates that 75 p.c of the rise in international manufacturing of liquid fuels from 2010 to 2019 got here from increased U.S. manufacturing. Slower productiveness progress and buyers’ demand for increased returns argue in opposition to a repeat efficiency within the years forward. The outcome could also be a persistently increased ground for international power costs.

Matthew Higgins is an financial analysis advisor in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Thomas Klitgaard is an financial analysis advisor in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How one can cite this submit:

Matthew Higgins and Thomas Klitgaard, “The Disconnect between Productiveness and Income in U.S. Oil and Fuel Extraction,” Federal Reserve Financial institution of New York Liberty Road Economics, August 17, 2022, https://libertystreeteconomics.newyorkfed.org/2022/08/the-disconnect-between-productivity-and-profits-in-u-s-oil-and-gas-extraction/.

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).