{kind=link}

A reader asks:

Lately my father handed away leaving roughly $150k to me as an inheritance and I’m attempting to determine if I ought to save or make investments it. I’m 26 years previous and served 4 years as a military officer. I will probably be separating honorably quickly the place I’ll return to highschool and should have to entry these funds. I additionally could use them to purchase a future home or get married. I’m afraid of investing the funds quick time period (lower than 3 years) in shares as volatility might affect negatively within the quick time period. CDs and a few bonds look like low returns when rate of interest are elevating (shouldn’t I wait to buy a CD if rates of interest will rise?). I did buy I bonds with a 9.62% rate of interest however I nonetheless don’t like the thought of the remainder of the cash sitting in a financial institution financial savings account yielding virtually nothing. Is sitting in money the most secure wager quick time period?

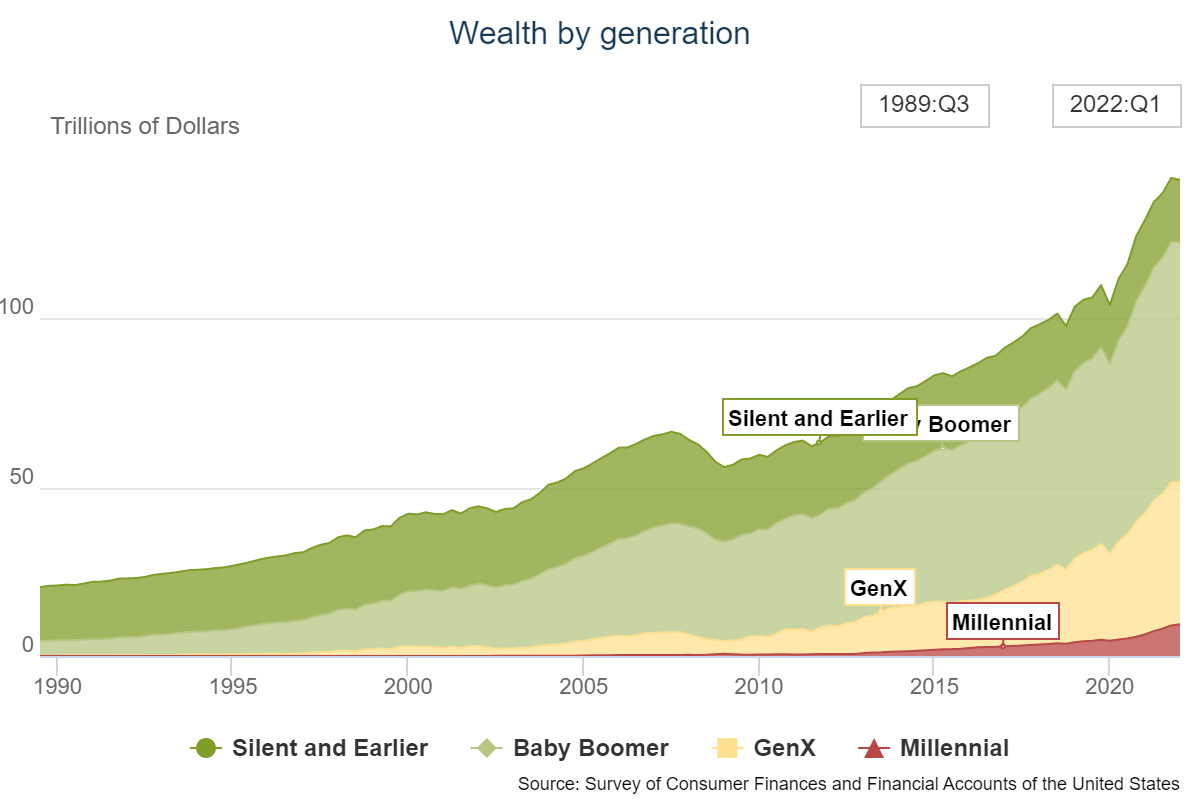

It’s sort of morbid to consider, however with some 70 million child boomers, there will probably be quite a lot of this occurring within the coming years.

The boomers are by far the wealthiest technology and quite a lot of that wealth goes to be handed right down to the following technology within the coming many years:

Cash is cash however for the reason that supply of this capital is coming out of your father’s demise I’m certain there may be going to be some extra emotional baggage connected to it.

You by no means need to screw up an enormous cash determination however the remorse potential could possibly be even greater once we’re speaking about an inheritance.

Fortunately, you have already got an thought of your threat profile and time horizon for these funds. That’s step one any time you’re investing new cash.

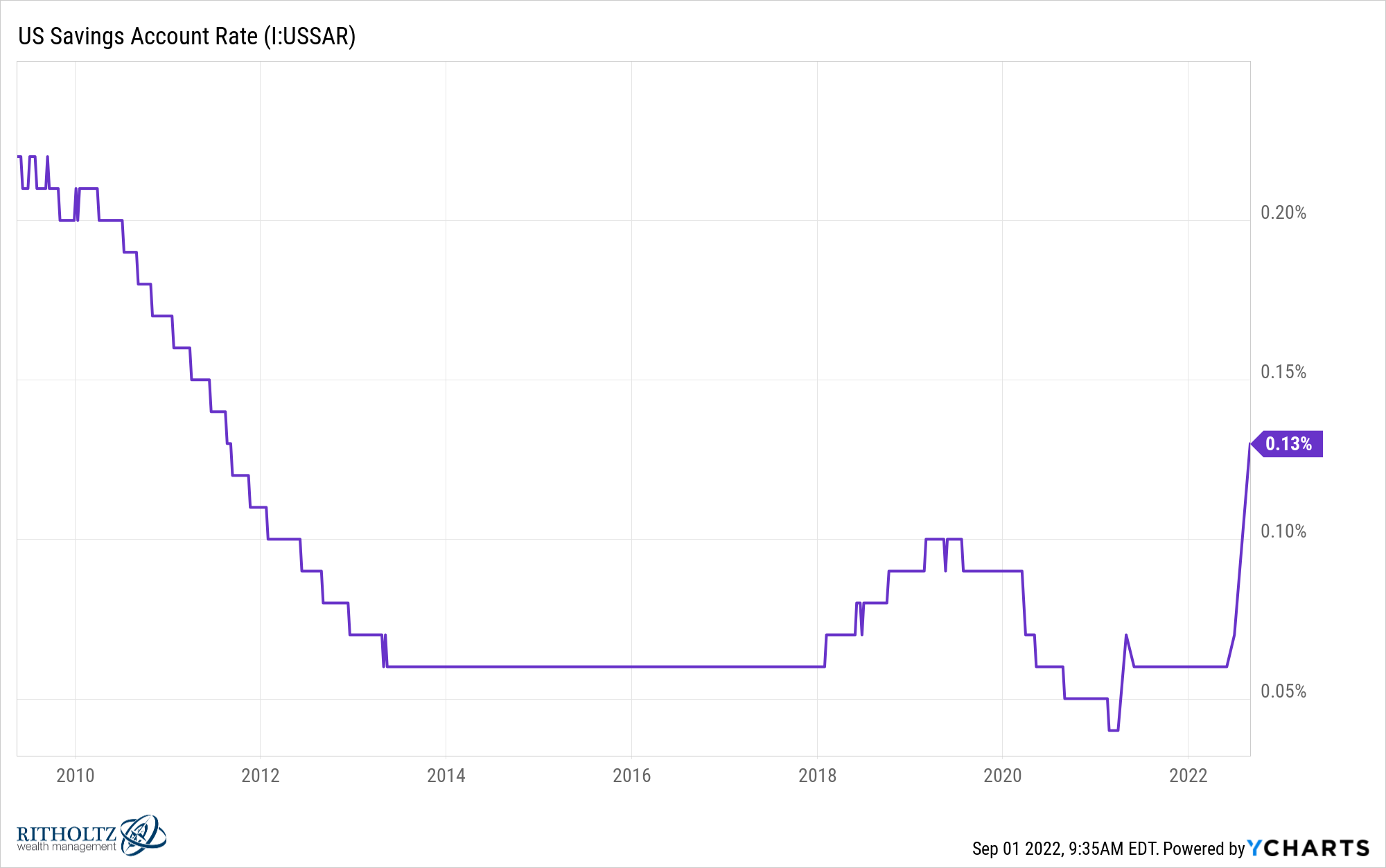

You’re additionally heading in the right direction to keep away from preserving this in a financial institution financial savings account. The common yield on a brick-and-mortar financial institution financial savings account continues to be atrocious:

It’s like they’re not even attempting anymore.1

The dangerous information is the Fed elevating rates of interest is probably going one of many causes the inventory market is falling and will push the financial system right into a recession.

The excellent news is savers like you possibly can lastly discover some yield on their money.

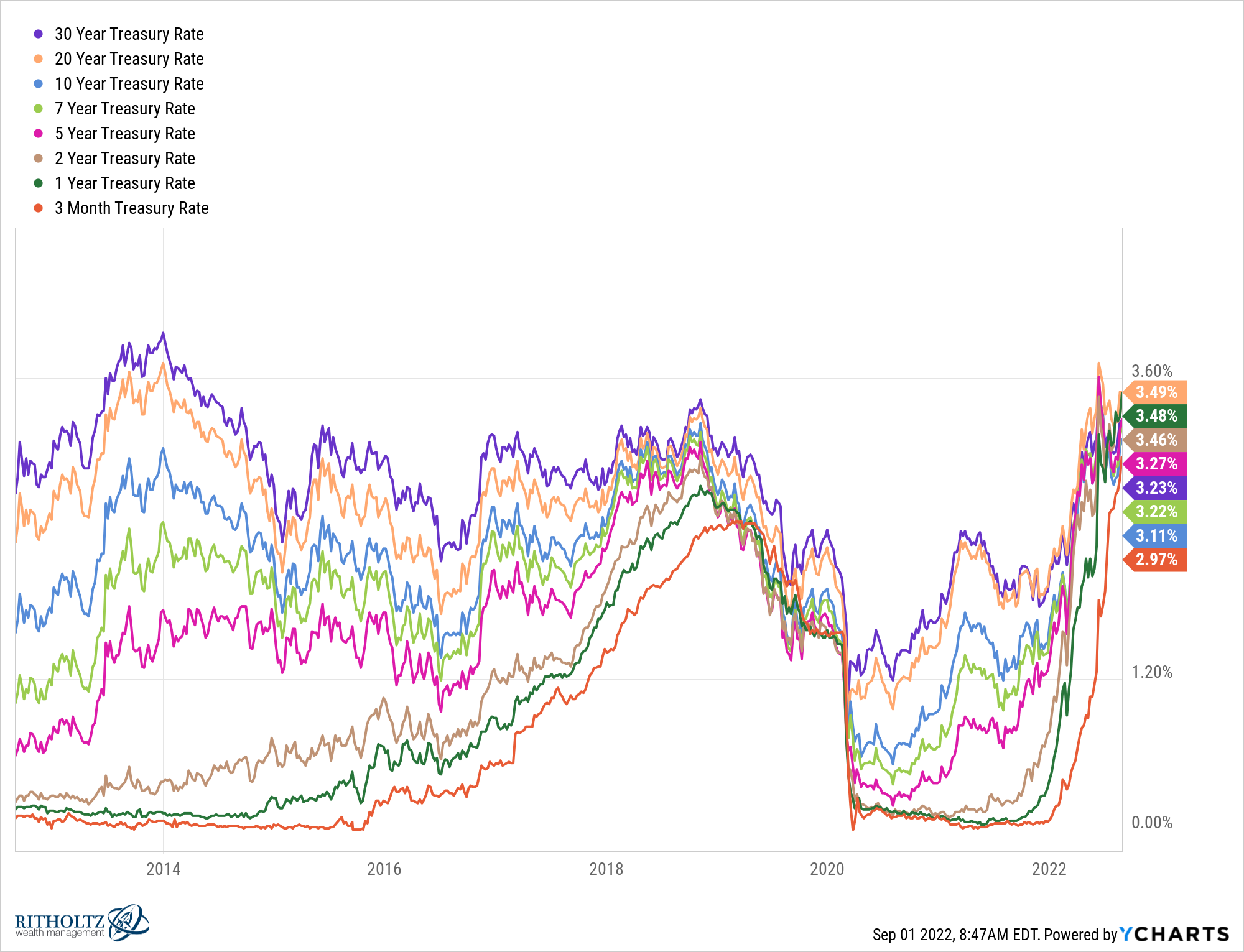

Simply take a look at the modifications in treasury charges this 12 months:

And it’s not simply that rates of interest are greater. The important thing right here for savers is that short-term rates of interest are a lot greater on an absolute and relative foundation.

One 12 months treasuries and 3-month t-bills are each up round 3% from their ranges initially of this 12 months. And these short-term bonds now yield mainly the identical as intermediate-term and long-term bonds.

Why does this matter?

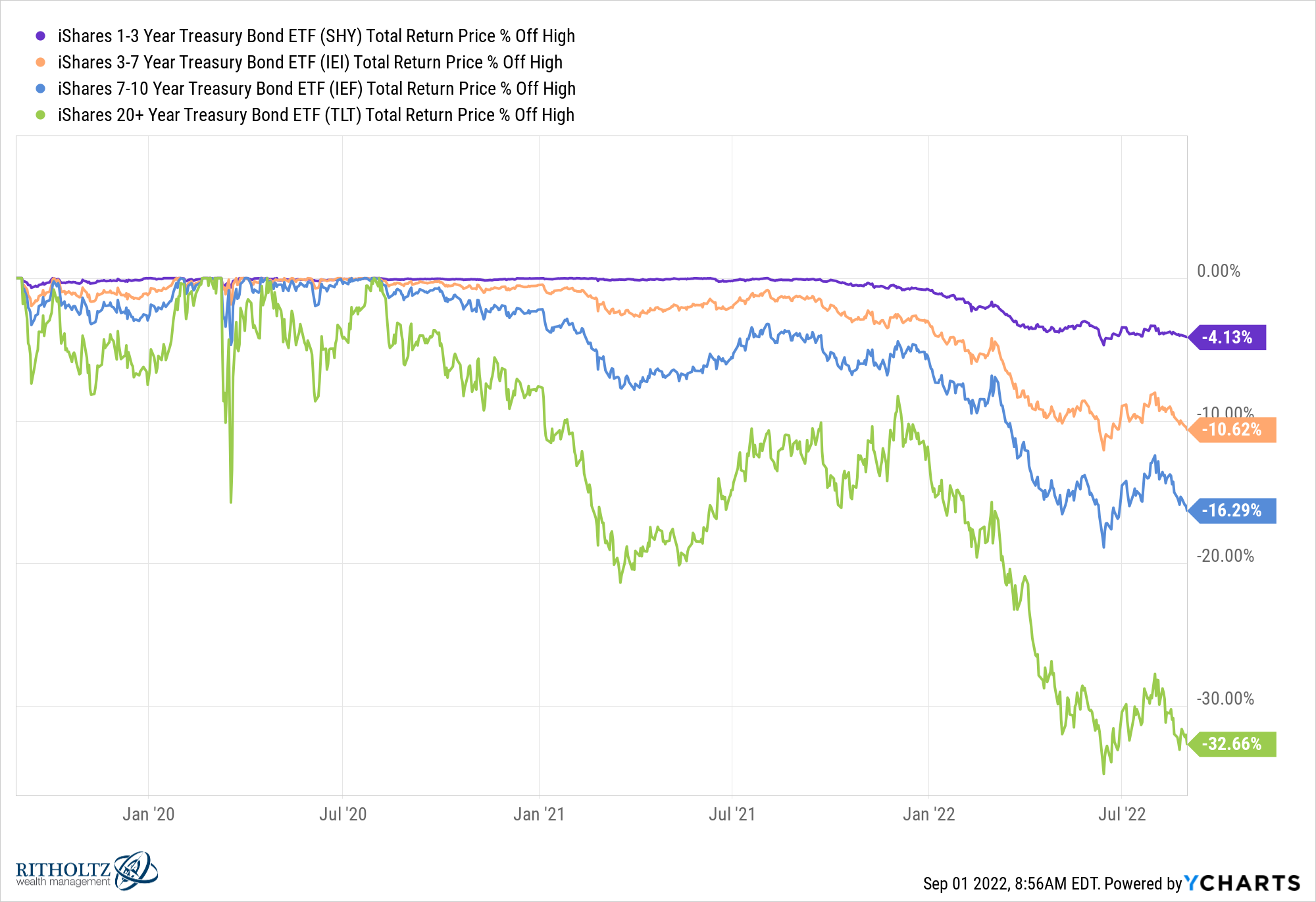

These bonds include decrease rate of interest threat. You may see in a rising charge atmosphere short-term bonds have held up significantly better than long-term bonds:

We’ve gone over this earlier than however as a refresher, all else equal, the longer the maturity of the bond (or bond fund) the extra variability to modifications in rates of interest. Nobody cares about variability when charges are taking place as a result of that’s a superb factor for bonds.

However when charges are going up that’s dangerous for bond costs. The longer your maturity the better the losses when charges rise.

For quite a few years the yields on short-term bonds have been paltry. Traders have been compelled to just accept extra threat to earn greater yields.

That’s not the case anymore.

It’s such as you’re being paid to take much less threat proper now by way of yield.

The iShares 1-3 12 months Treasury Bond ETF (SHY) now sports activities a mean yield to maturity of three.5%. That’s greater than the yield on a 30 12 months treasury bond (and my present mortgage charge…to not brag).

A yield of three.5% continues to be comparatively low in comparison with historic rates of interest of the previous 50-60 years however in comparison with the previous 10 years it’s an enormous improve.

On a tax-equivalent foundation, municipal bonds supply an analogous charge.

The iShares Brief-Time period Nationwide Muni Bond ETF (SUB) has a yield to maturity of two.4%. In the event you have been within the 25% tax bracket, the tax-equivalent yield on that might be 3.2% (assuming you’re holding these in a taxable account).

Once more, not dangerous.

The web financial savings accounts are even lastly beginning to improve their charges. Marcus is 1.7%. Ally is 1.85%. Capital One is 1.75%. These yields ought to go greater if the Fed continues to hike.

You may’t precisely transfer to the seashore and dwell off the curiosity on yields of 2-3% nevertheless it’s higher than nothing, which is what savers might earn the previous couple of years in a world of 0% rates of interest.2

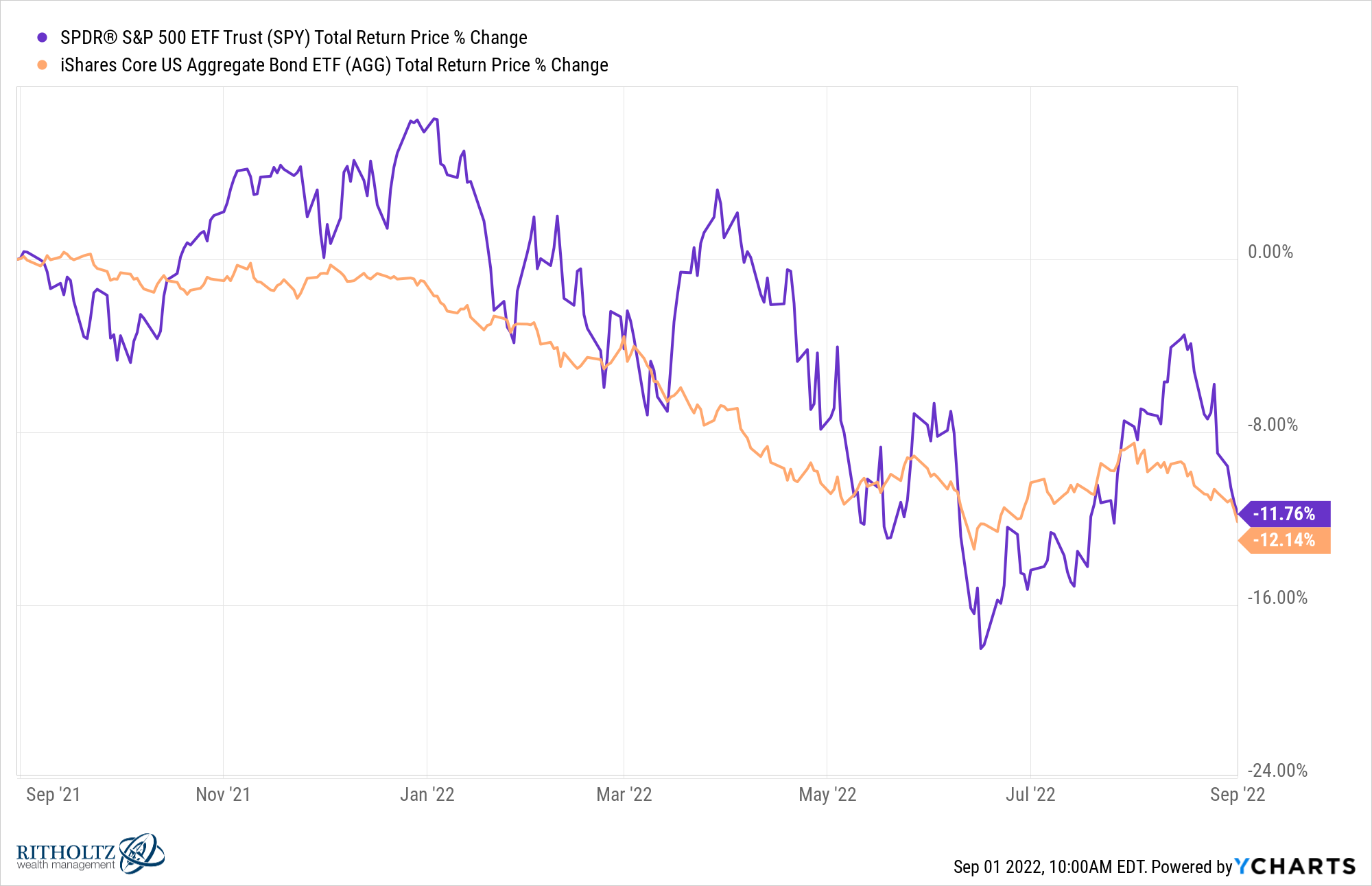

From an asset allocation standpoint, it will likely be attention-grabbing to see if money catches a bid from traders. U.S. shares and U.S. bonds are each down 12% or so prior to now 12 months:

With short-term bonds and money equivalents lastly providing some yield it’s doable extra traders will merely park their cash there for some time.

Surprisingly, money beats shares and bonds in a given 12 months extra typically than you’d suppose.

Over the previous 94 years, money (3-month t-bills) has overwhelmed the inventory market (S&P 500) in additional than 30% of all calendar years. Money has overwhelmed bonds (10 12 months treasuries) greater than 40% of the time.

And money has overwhelmed each shares and bonds in the identical 12 months 1 out of each 8 years, on common.

So it’s not out of the extraordinary for money to be king, at the very least within the short-term.

This doesn’t really feel like an amazing factor for traders in threat belongings proper now.

However savers of the world rejoice. You may lastly earn an honest yield in your money.

We mentioned this query on the newest version of Portfolio Rescue:

Invoice Candy joined me as effectively to speak about going from two incomes right down to a single-income household, pre-paying school bills, rolling over a 401k to a Roth IRA, paying taxes in retirement, the tax affect of scholar mortgage forgiveness and extra.

Additional Studying:

Historic Returns For Shares, Bonds & Money Again to 1928

Right here’s the podcast model of right this moment’s present:

1With the Fed Funds Charge north of two% (and going greater) and mortgage charges at 6% this needs to be unlawful.

2Excessive inflation doesn’t precisely assist right here both however these charges are a begin.