{kind=link}

ABSLI Fastened Maturity Plan provides you look-and-feel of a financial institution mounted deposit however disappoints on the returns entrance. Low assured returns. Membership this with the untimely exit penalty and this product turns into a simple keep away from.

We love Financial institution mounted deposits. Nearly 2/3rd of Indian family wealth is in financial institution mounted deposits. Thus, it’s logical for an insurance coverage firm to launch merchandise that provide you with look-and-feel of a financial institution mounted deposit. Aditya Birla Solar Life Insurance coverage has launched ABSLI Fastened Maturity plan.

How is ABSLI Fastened Maturity plan much like a Financial institution FD?

- Comparable nomenclature (There’s “Fastened” within the plan title)

- Single Premium (very like your FD funding)

- Assured returns (recognized upfront)

- Simple calculation of maturity quantity

- Not very lengthy maturity (5-10 years)

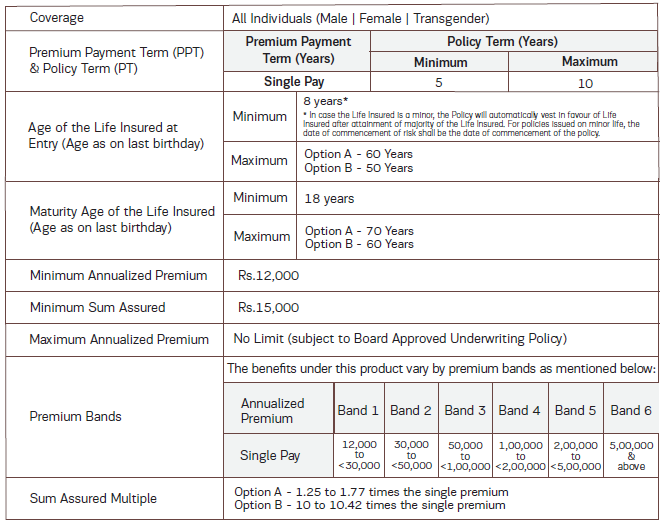

ABSLI Fastened Maturity Plan: Vital Options

ABSLI Fastened Maturity plan is a non-participating plan. With non-participating plans, upfront how a lot you’re going to get and when. Assured returns. Due to this fact, you should use any spreadsheet software program to calculate the IRR (returns). Underneath any non-participating plan, it’s the legal responsibility of the insurer to pay you the promised quantities.

Single Premium.

2 Variants. Choice A and Choice B.

Maturity proceeds from Choice A shall be taxable because the Sum Assured is lower than 10 instances single premium.

Maturity proceeds from Choice B shall be exempt from tax.

Coverage time period of 5 to 10 years. Therefore, not a really lengthy maturity product. ABSLI has tried to place this product as an alternative choice to a long-term FD.

I reproduce the desk from the product brochure.

What would be the returns like?

Since it’s a non-participating plan, upfront what you’re going to get.

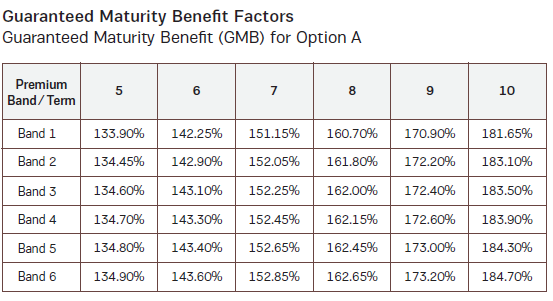

You get assured maturity profit (GMB). We are going to first take a look at returns from Choice A after which take a look at Choice B.

With this info, you may simply calculate your returns.

Let’s say you’re 45 years outdated.

Funding: Rs 10 lacs. Together with GST, you’ll pay 10.18 lacs.

Choice A.

Maturity: 5 years.

Because the premium is greater than Rs 5 lacs, you fall in Band 6.

On completion of 5 years, you’re going to get 134.9% of your funding quantity i.e., 13.49 lacs. That’s an IRR of 6.17% p.a.

Had you opted for coverage time period of 10 years, you’d have gotten 184.7% i.e., 18.47 lacs again. 6.33% p.a.

Nevertheless, that is Choice A. Your returns are taxable.

Let’s strive the identical mixtures with Choice B.

Funding: Rs 10 lacs. Together with GST, you’ll pay 10.18 lacs.

Choice B.

Maturity: 5 years.

You’ll get 126.55% again i.e., 12.65 lacs again on completion of 5 years. That’s an IRR of 4.82% p.a.

Change coverage time period to 10 years.

You’ll get 168.35% again or 16.83 lacs on completion of 10 years. IRR of 5.35% p.a.

With Choice B, your returns are tax-free.

Your entry age will have an effect on your returns

In non-participating plans (and even taking part plans and ULIPs), the return will depend on your entry age. Every part else being the identical, a 35-year-old (on the time of entry) will earn higher returns than a 45-year-old.

Why does this occur?

Simply take a look at the GMB numbers for Choice B. The GMB goes down with age.

For Choice A, because the Sum Assured is just one.25 to 1.77 instances the Single Premium, your age doesn’t have an effect on the returns (that’s the way in which plan is structured).

Nevertheless, for Choice B, the Sum Assured is 10 instances the Single premium. A much bigger portion of the premium will go in direction of offering life insurance coverage cowl. And value of life insurance coverage is greater for older buyers. Thus, you may see GMB values go down with entry age for Choice B. And that ensures that decrease returns for greater entry age.

For the examples thought-about (45-year-old).

Choice A provided IRR of 6.17% p.a. and 6.33% for coverage tenures of 5 and 10 years respectively. Taxable. The returns gained’t change with entry age.

Choice B provided IRR of 4.82% p.a. and 5.35% for coverage tenures of 5 and 10 years respectively. Tax-free. For a 35-year-old, IRRs enhance to five.40% (5-year coverage time period) and 5.59% p.a.

An FD (or any pure funding product) provides the identical return no matter age.

It’s essential to additionally see that Choice A provides higher returns than Choice B

Whereas that is evident from the illustrations, why does this occur?

Once more, the price of life insurance coverage.

Because the Choice A covers you for 1.25XSingle Premium, your funding incurs decrease price for all times insurance coverage.

Choice B is at the least 10X Single Premium. Larger insurance coverage price. Decrease returns.

Therefore, every part else being the identical, Choice A will supply higher returns than Choice B.

However maturity profit from Choice A is taxable. Exempt for Choice B

Why?

As a result of the Sum Assured in Choice A is just one.25 to 1.77 instances single premium.

As per earnings tax legal guidelines, the maturity proceeds from insurance policy are exempt from tax provided that the Sum Assured (Life cowl) is at the least 10 instances the annual premium.

For tax exempt returns, Sum Assured >= 10 instances Annual (or Single premium).

Choice A doesn’t meet the situation. Solely Choice B does.

Choice A: Larger however taxable returns. You’ll pay tax solely on the returns (not on the principal). To be taxed at your marginal fee.

Choice B: Decrease however tax-free returns.

In case you are planning to take a position, test the post-tax returns.

We often affiliate life insurance coverage merchandise with tax-free returns. In case you are contemplating ABSL Fastened Maturity plan as an alternative choice to a financial institution mounted deposit due to tax-free returns, you’ll be disillusioned with choice A.

Untimely exit is expensive

Conventional plans (and non-participating plans are not any completely different) have inflexible exit necessities. Whereas this plan permits you to give up the plan after your funding, you’re going to get a really small quantity again.

For example, in case of give up, you’re going to get the upper of the next two again.

- Assured Give up Worth (GSV) = GSV issue X Single Premium Paid. The GSV issue matrix will not be supplied within the coverage doc or brochure. Guess I should purchase the plan to determine this out.

- Particular give up worth (SSV) = The maturity proceeds discounted at 30-year G-sec fee + 2%. The 30-year G-sec yield as on August 8, 2022, is 7.7% p.a. The maturity worth shall be discounted at 9.7% p.a. Now, this may be calculated.

For a 45-year-old, Choice B returned 16.83 lacs after 10 years on funding of Rs 10.18 lacs (consists of 18K GST).

In the event you give up a number of days later, you’re going to get 16.83 lacs/ (1+9.77%) ^10 = Rs. 6.62 lacs again. You had invested 10.18 lacs.

With a financial institution mounted deposit, you’ll not have such an issue. Solely a minor curiosity penalty.

What do you have to do?

ABSLI Fastened maturity provides the look-and-feel of a financial institution mounted deposit product.

Assured returns (until you assume ABSLI can default).

Not very lengthy maturity.

And I need to say that the plan has a quite simple construction. I’ve reviewed many non-participating plans earlier. Whilst you can work out what you’re going to get with these plans too, these plans are likely to have very difficult calculations. Simply take a look at LIC Dhan Sanchay (Plan 865) that I reviewed not too long ago. ABSLI Fastened Maturity plan is kind of crisp. Maturity worth is a straightforward proportion of your single premium. Similar to a financial institution FD.

Nevertheless, the product doesn’t impress on the returns entrance. Choice A has greater however taxable returns. Choice B has tax-free however decrease returns. Neither variant is nice sufficient.

Furthermore, the returns rely in your entry age, leading to decrease returns for older buyers. Untimely exit is pricey.

Counsel you give this product a go.

In the event you discover benefit on this product, do think about the tax implications of Choice A and Choice B earlier than selecting between the 2. It’s simple to disregard that returns from Choice A shall be taxable.