{kind=link}

Govt Abstract

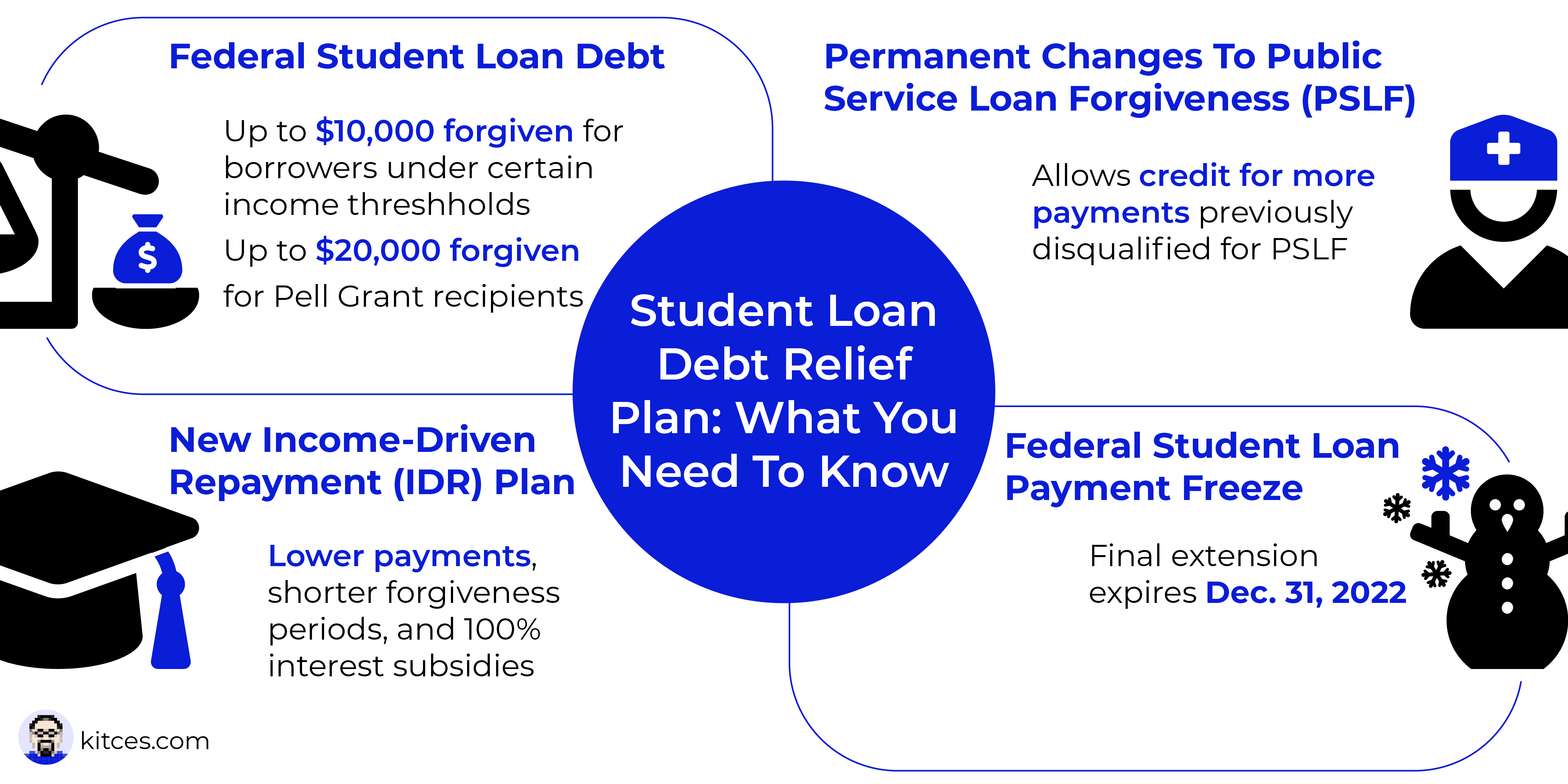

The Biden administration’s long-anticipated Pupil Mortgage Debt Reduction plan was lastly introduced on August 24, 2022, and with it got here a flurry of consideration on the proposal’s centerpiece of offering $10,000 of pupil mortgage forgiveness for Federal pupil mortgage debtors (and $20,000 for debtors who acquired a Pell Grant for school) with earnings ranges beneath $125,000 for single debtors and $250,000 for married {couples}.

However pupil mortgage forgiveness is only one a part of the administration’s plan for pupil debt aid. Along with the $10k – $20K of potential forgiveness, the plan additionally supplies one other (remaining) extension to the pause on Federal pupil mortgage funds till December 31, 2022; a push for debtors who could also be eligible for the Public Service Mortgage Forgiveness (PSLF) Waiver to use for the waiver earlier than its expiration on October 31, 2022 (together with some important adjustments to the eligibility necessities for PSLF going ahead); and the creation of a brand new Revenue-Pushed Compensation (IDR) plan that might decrease month-to-month funds and doubtlessly cut back the time interval required for mortgage forgiveness for eligible debtors.

Whereas elements of the administration’s plan will occur routinely (as an illustration, many debtors with IDR plans who’ve already recertified their earnings with the U.S. Training Division, not like different debtors who’ve but to take action, can be routinely eligible for his or her mortgage forgiveness), different elements might require extra motion. For instance, debtors who’ve made funds on their loans for the reason that pause on pupil mortgage funds began in March of 2020 might need to request a refund of these funds – as a result of though a refund will finish out rising the borrower’s mortgage steadiness, it may additionally lead to a larger quantity of debt forgiven, whereas permitting the borrower to easily ‘preserve’ their refunded funds!

Consequently, for monetary advisors, an in-depth understanding of the small print of the Biden administration’s pupil mortgage aid proposal will make it potential to offer useful recommendation to their purchasers on how these adjustments will work in actual life, how they are going to work together with the consumer’s broader monetary circumstances, and tips on how to maximize the potential advantages obtainable.

For purchasers with pupil loans, advisors will help them perceive how a lot debt they may qualify to have forgiven, maximize any forgiveness routes that could be obtainable to them, and plan for a way pupil mortgage forgiveness will impression their longer-term monetary image. Moreover, for purchasers eligible for PSLF, advisors will help guarantee they’re receiving correct credit score for his or her service beneath the brand new Waiver’s provisions, and doubtlessly apply for credit score beneath the Waiver earlier than its expiration date on October 31, 2022. And for purchasers on IDR plans, advisors will help their purchasers decide their eligibility for the brand new IDR plan and the way it will examine with their present IDR plan. Lastly, for all Federal mortgage debtors, advisors will help their purchasers put together for the impression on their money stream of pupil mortgage funds resuming in January 2023 after a virtually 3-year moratorium on funds and curiosity.

The important thing level is that as a result of the Biden administration’s proposal could have such broad-reaching results on debtors with Federal pupil loans, the plan represents a terrific alternative for advisors to attach with purchasers who’ve such loans (or who’ve members of the family with pupil loans). In the end, almost each Federal pupil mortgage borrower could also be affected – hopefully positively – by a minimum of one of many plan’s provisions and, given the impression of pupil loans on the conditions of so many people (each when it comes to monetary standing and psychological well-being), advisors can present immeasurable worth in guiding purchasers by way of these adjustments!

Authors:

One of many key guarantees of Joe Biden’s presidential marketing campaign in 2020 was that pupil mortgage debtors could be supplied some aid, together with a pledge to cancel a minimal of $10,000 of pupil debt per particular person. However that pledge went unfulfilled for the primary 12 months and a half of Biden’s presidency, main many to wonder if altering political winds had dampened the president’s enthusiasm for what would have been an unprecedented step towards lowering the $1.7 trillion of excellent Federal pupil mortgage debt.

On August 24, 2022, nevertheless, the Biden administration lastly took some long-awaited motion on its promise, saying a sweeping pupil mortgage aid program that, amongst different issues, forgives as much as $10,000 of pupil mortgage debt for debtors (and as much as $20,000 of forgiveness for Pell Grant recipients) beneath sure earnings thresholds.

Pupil Mortgage Debt Reduction Plan: Key Provisions

Whereas pupil mortgage forgiveness has been the principle focus of most of the headlines saying the Pupil Mortgage Debt Reduction Plan, the administration’s proposal bundles collectively a number of key provisions that even have relevance to present and future pupil mortgage debtors.

At a excessive degree, these provisions embody:

- Cancellation of pupil mortgage debt:

- As much as $10,000 for debtors with earnings beneath $125,000 for single people and $250,000 for married {couples};

- As much as $20,000 for Pell Grant recipients, with the identical earnings thresholds as above;

- One other (remaining) extension of the pause on Federal pupil mortgage funds by way of December 31, 2022;

- A number of the adjustments initially made by the Public Service Mortgage Forgiveness (PSLF) Waiver will change into everlasting provisions of PSLF, even after the waiver ends on October 31, 2022, and can be publicized by way of an consciousness marketing campaign geared toward eligible people. These adjustments will contain permitting credit score for late or lump sum funds and for deferment or forbearance for folks with qualifying employers (e.g., Peace Corps, army deployment); and

- Creation of a newly proposed Revenue-Pushed Compensation (IDR) plan that limits funds on Federal undergraduate loans to five% of the borrower’s discretionary earnings and forgives loans of lower than $12,000 after 10 years of funds.

These adjustments are being carried out by way of government motion reasonably than by way of legislative passage, which means that, not like proposed laws that usually undergoes many transformations whereas winding by way of committees and debate in each homes of Congress, there are much less prone to be substantial adjustments to the Biden administration’s proposal earlier than its implementation (aside from filling in particulars which have but to be introduced). Nonetheless, there’s a important likelihood that Republicans who oppose the plan will attempt to cease its implementation with authorized challenges, which means that the final word end result is perhaps decided by the courts.

Nonetheless, with an estimated 43 million pupil mortgage debtors in the US – to not point out different stakeholders like spouses, dad and mom, youngsters, and employers who’re additionally affected by a borrower’s pupil mortgage debt – the aid plan has the potential to impression an enormous variety of households, together with the purchasers of many monetary advisors. And though most of the plan’s ‘high quality print’ particulars have but to be launched, advisors can nonetheless play a important position in serving to their purchasers to begin planning now to verify they will profit from these proposals to the best extent potential, and to be ready for motion on the extra time-sensitive parts when the proposal is finalized.

Cancellation Of Up To $10,000 Or $20,000 In Pupil Federal Mortgage Debt

Though advocates for aid had been pushing the Biden administration to forgive as a lot as $50,000 of pupil debt per borrower, the administration finally settled on decrease however nonetheless substantial most forgiveness quantities. Extra particularly, debtors who qualify and are beneath sure earnings thresholds (mentioned later) can be restricted to a most forgiveness quantity of $10,000. And for debtors who have been recipients of Federal Pell Grant awards, the utmost quantity of mortgage forgiveness is doubled to $20,000.

Though future steering from the U.S. Division of Training may lead to a special end result, the entire quantity of a person’s Pell Grant doesn’t at the moment appear to be a think about calculating the utmost forgiveness quantity. Somewhat, receipt of any quantity of Pell Grant funding seems to be sufficient to entitle a borrower to the $20,000 restrict.

Notably, the mortgage forgiveness for debtors who acquired Pell Grants isn’t supposed to repay the Pell Grants themselves (which usually don’t should be repaid besides beneath sure circumstances). Somewhat, since Pell Grants are usually supplied solely to college students with “distinctive monetary want,” they function a tough ‘measuring stick’ for debtors with larger monetary want and/or fewer private or household assets obtainable to pay down their debt.

Eligibility For Forgiveness Is Based mostly On Taxpayer Revenue Ranges

Whereas many debtors will qualify for the utmost quantity of forgiveness ($10,000 of pupil mortgage debt, or $20,000 of pupil mortgage debt for Pell Grant recipients), many high-income taxpayers won’t be eligible for the aid. In fact, that begs the query, “Who’s a high-income taxpayer?”

The White Home Reality Sheet signifies that the earnings threshold to qualify for forgiveness is $125,000 for single filers and $250,000 for married {couples}, whereas a press launch by the U.S. Division of Training clarified that the $250,000 threshold additionally applies to Head of Family filers. Whereas different submitting statuses should not talked about, all indications recommend that they may also be topic to the person $125,000 threshold quantity, together with married {couples} who file individually (which might be significantly important for the big variety of married debtors utilizing sure IDR compensation methods, who file individually as a way to cut back their month-to-month mortgage funds).

Whereas it seems that no definition of “earnings” has but been publicly formalized, Revenue-Pushed Compensation (IDR) Plans usually use a person’s Adjusted Gross Revenue (AGI) for comparability to the Federal Poverty Restrict earnings. Accordingly, AGI would appear to be the main candidate for the definition of earnings right here, as effectively.

One factor we do know for sure, nevertheless, is when earnings issues… or, extra appropriately, when it mattered. Whereas neither the White Home Reality Sheet nor the U.S. Division of Training Press Launch makes any reference to particular dates, an administration official did affirm throughout a White Home Press briefing that the related tax years of a borrower’s earnings are 2020 and 2021.

The excellent news for debtors hoping for aid is that the identical official confirmed that, though the measuring years are 2020 and 2021, it’s not crucial for earnings to be under the thresholds in each years. Somewhat, so long as a person’s earnings was under their relevant threshold in both 2020 or 2021, they are going to qualify for the aid.

Instance 1: Bryan is a single taxpayer and has $20,000 of excellent pupil loans (he was not a Pell Grant recipient).

In 2020, Bryan received $100 million within the lottery.

In 2021, he labored and had an AGI of $124,999.

Since Bryan’s AGI in 2021 was under the $125,000 threshold for single filers, he can be eligible for $10,000 of pupil debt forgiveness from the Pupil Mortgage Debt Reduction Plan.

The unhealthy information for some debtors, nevertheless, is that every one indications appear to level in the direction of the earnings thresholds being ‘cliff’ thresholds. In different phrases, so long as a person’s earnings is under their specific threshold, they will qualify for the total quantity of aid. However upon reaching the edge, their whole profit – as much as $10,000, or $20,000 for Pell Grant recipients – is eradicated (just like the best way Medicare Half B/D Revenue-Associated Adjustment Quantities [IRMAAs] work).

Notably, the White Home Reality Sheet additionally states that “No particular person making greater than $125,000 or family making greater than $250,000 – the highest 5% of incomes in the US – will obtain aid.” This would appear to offer robust proof that people with only a single greenback of earnings over the edge would ‘fall off the cliff’ and obtain no profit in any respect.

Instance 2: Adam is Bryan’s fortunate twin brother and can also be a single taxpayer with $20,000 of excellent pupil loans.

In 2020, Adam additionally received $100 million within the lottery.

In 2021, Adam labored and had wages of $124,999, however he additionally received $5 on a scratch-off lottery ticket, which he diligently reported, bringing his AGI to $125,004.

Since Adam’s AGI was not under the edge for single filers in both 2020 or 2021, he’ll not obtain any pupil debt forgiveness from the Pupil Mortgage Debt Reduction Plan.

Using a cliff threshold may create very attention-grabbing dynamics for some debtors. In some circumstances, a couple of additional {dollars} of earnings may, in hindsight, be the explanation a person did not qualify for aid. And in different circumstances, debtors who earned much less in 2020 or 2021 may really find yourself in superior monetary positions (as Bryan did in Instance 1 above)!

Revenue-Tax Penalties Of Forgiveness

Usually, when a person has debt discharged, the forgiven debt turns into taxable earnings. Presently, nevertheless, due to adjustments made by the American Rescue Plan Act of 2021, most pupil debt discharged by way of 2025 (together with any debt forgiven by the president’s present proposal) can be tax-free… a minimum of on the Federal degree.

On the state degree, although, earnings tax penalties are a complete totally different ball recreation. In states with no earnings tax or the place state earnings tax guidelines conform to Federal guidelines, such discharged debt may also be tax-free on the state degree. However for some states that do not conform to Federal tax regulation, the forgiven debt can be taxable on the state degree. At the very least for now.

Given the broad nature of the aid supplied by the Biden administration, some states that might usually tax forgiven debt might select to cross laws (which they might select to make non permanent or everlasting) to make such forgiven debt tax-free on the state degree as effectively. Accordingly, debtors ought to keep watch over their state legislators.

Planning Methods To Qualify For Forgiveness

Utilizing 2020 and 2021 because the measuring years implies that for many debtors, at this level, there is no such thing as a planning that may be executed to qualify for mortgage forgiveness. Both their earnings was under the relevant threshold throughout these years, or it wasn’t. Nonetheless, for people who did not qualify primarily based on their 2020 earnings however haven’t but filed their 2021 tax returns, there are nonetheless a restricted variety of planning methods that would assist them to qualify for forgiveness.

First, to the extent a person is a enterprise proprietor and nonetheless has the power to make deductible contributions to a retirement plan for 2021 (e.g., a self-employed particular person contributing to their very own SEP IRA), if these contributions, and the corresponding deductions, cut back AGI sufficient to get beneath the relevant threshold, such contributions ought to be rigorously thought-about.

As well as, if the thresholds for single filers are additionally utilized to married people who file separate returns, married {couples} with pupil debt ought to consider whether or not submitting separate returns for 2021 is smart, even when they usually file joint returns. If the debt forgiveness obtainable to at least one partner exceeds the extra tax burden (plus every other relevant prices, equivalent to tax prep charges) created by submitting individually, it might be a internet win.

Varieties Of Loans Which Qualify For Forgiveness

Usually, solely Federal loans which have been funded by June 30, 2022, are eligible for forgiveness, as introduced by the Biden administration. Nonetheless, present debt (as of June 30, 2022) that was consolidated after the deadline remains to be eligible for aid.

Conversely, privately held pupil loans are usually not eligible for a similar aid, whatever the borrower’s degree of earnings. This raises considerations for a lot of debtors with Federal Household Training Loans (FFELs), that are Federally backed loans initially funded by non-public firms. When these loans have been initially issued, some have been subsequently bought by the Federal authorities, whereas others remained beneath the possession of personal firms. And whereas FFELs owned by the U.S. Division of Training will be eligible for forgiveness, it’s not but clear how loans held by non-public firms can be handled.

Initially, it was believed that all privately held debt, together with these FFELs owned by non-public firms, could be ineligible for forgiveness (aligning with present steering on forbearance and the 0% rate of interest). Nonetheless, the Division of Training has indicated a want to increase forgiveness to these debtors whose FFEL loans are owned by non-public firms, both immediately or by way of loans which are consolidated to Direct Federal loans. Affected debtors (and their advisors) are inspired to pay shut consideration to those developments.

To the shock of many, Federal loans taken out for graduate college are eligible for aid, as are Mother or father Plus Loans. Notably, most debt aid seems to narrate to the borrower – not the scholar. Thus, dad and mom with $30,000 of complete Mother or father Plus loans unfold out evenly over three youngsters will ‘solely’ be eligible for a most of $10,000 of forgiveness. Against this, if a pupil’s dad and mom had $10,000 of Mother or father Plus loans for his or her baby’s training, and the kid had an extra $20,000 and had acquired a Pell Grant, a most of $30,000 of debt associated to that pupil’s training might be eradicated ($10,000 for the dad and mom and $20,000 for the scholar).

Lastly, it is price noting that present college students with debt are eligible for aid as effectively. Nonetheless, if the scholar is at the moment claimed as a depending on their dad and mom’ earnings tax return, their dad and mom’ earnings can be used to find out eligibility.

Making use of To Obtain Mortgage Forgiveness

For some debtors, the forgiveness course of goes to be comparatively straightforward. Notably, roughly 8 million pupil mortgage debtors have already got earnings info on file with the U.S. Division of Training (e.g., debtors who’re on an Revenue-Pushed Compensation plan choice) that may enable them to routinely obtain forgiveness. However anybody who’s on an IDR Plan who has not but submitted earnings info for 2020 or 2021 (as they weren’t required to) nonetheless wants to use and submit proof of their earnings as a way to qualify.

For others, the completion of a (purportedly) easy software can be crucial. The White Home has directed the Division of Training to make the appliance obtainable no later than the top of 2022, however the Division of Training has acknowledged it intends to launch the appliance sooner than that, “within the coming weeks.”

Debtors who need updates immediately from the U.S. Division of Training can signal as much as obtain them by visiting https://studentaid.gov/debt-relief-announcement/.

Pupil Mortgage Fee Freeze Ending In December 2022

Debtors of Federal pupil loans have benefitted from a brief moratorium on pupil mortgage funds and curiosity for the reason that early days of the COVID-19 pandemic, when former President Donald Trump issued an government order in March 2020 first establishing the fee freeze. Subsequent extensions extended it for greater than 2 ½ years, and although the freeze was set to run out on the finish of August 2022, the Biden administration’s Pupil Mortgage Debt Reduction Plan has added one remaining extension to the fee freeze, pushing the top date again 4 months from August 31 to December 31, 2022.

However, not like earlier cases when ‘remaining’ extensions have been introduced solely to be re-extended additional, the mixture of this extension with the debt aid bundle makes it appear seemingly that this actually will be the top of the road, and that Federal pupil mortgage debtors will resume their funds in January 2023 after almost three years of frozen funds and 0% curiosity.

Refunds Of Funds Made Throughout The Momentary Fee Freeze Can Doubtlessly Improve Forgiveness Quantity

When the CARES Act handed in March 2020, it included a clause that allowed debtors to ask for a refund of any funds made after March 13, 2020, when the fee freeze was first introduced. This messaging remains to be clearly laid out on the U.S. Division of Training’s web site, which states:

You will get a refund for any fee (together with auto-debit funds) you make through the fee pause (starting March 13, 2020). Contact your mortgage servicer to request that your fee be refunded.

As of this writing, this coverage remains to be in impact and might create a possible planning alternative for a portion of the roughly 1.5% of debtors who continued to make voluntary funds through the moratorium. Extra particularly, debtors whose voluntary funds made after March 2020, after the passage of the CARES Act, lowered their excellent mortgage steadiness under their most forgiveness quantity may request a refund of such funds to extend their excellent debt. Which implies that, to the extent the elevated debt stays under their most forgiveness quantity, there’s a risk that it could qualify for forgiveness!

Instance 3: Josh is a single taxpayer with earnings in 2021 that was under his relevant $125,000 threshold. He had $26,000 of excellent Federal pupil loans as of March 2020. Josh selected to maintain paying down his debt to reap the benefits of the 0% curiosity.

As of August 2022, Josh’s excellent steadiness is $2,500. Absent any additional motion on Josh’s half, he can be eligible to have his remaining $2,500 (the lesser of his mortgage steadiness and $10,000) of pupil mortgage debt forgiven by the Pupil Mortgage Debt Reduction Plan.

Suppose, nevertheless, that Josh calls his mortgage servicer and asks for a refund of his funds made since March 2020. By doing so, he’ll obtain a refund of the $26,000 – $2,500 = $23,500 in funds he made through the fee freeze, and his mortgage steadiness would improve again to $26,000 (the steadiness when the scholar mortgage fee freeze started).

If Josh had acquired a Pell Grant whereas he was an undergraduate, he would possibly now be eligible for $20,000 of forgiveness. Which might imply that when his $20,000 of forgiveness is processed, his remaining mortgage steadiness due would solely be $26,000 – $20,000 = $6,000. Whereas that is $6,000 extra debt than he would have been left with if he had merely continued paying his debt right down to zero, by requesting the refund and qualifying for forgiveness, he’ll as a substitute have $23,500 extra in his checking account, making it a significantly better end result!

To be clear, this technique, if viable (extra on this under), would solely be useful to those that have made voluntary pupil mortgage funds since March 13, 2020, and who had earnings in 2020 or 2021 under their relevant threshold, and who at the moment have mortgage balances under their most forgiveness quantity. Whereas that group of taxpayers could also be small, the potential windfall they might see makes this an vital technique for advisors to grasp.

To implement this method, people assembly the circumstances described above ought to name their mortgage servicer to request a refund of these funds. Mortgage servicers will add any quantities paid down after March 13, 2020, again to the borrower’s excellent mortgage steadiness, and the borrower will obtain a refund in roughly 30-45 days.

Critically, for advisors discussing this method with purchasers, it’s vital to emphasise that it’s not but clear whether or not this technique will work. Extra particularly, the Division of Training might restrict forgiveness to the excellent steadiness as of the date of the announcement. In the event that they do take such an method, subsequent will increase in mortgage balances on account of refunded funds might be ineligible for aid.

That being mentioned, it may nonetheless be worthwhile for debtors to request a refund of any post-freeze funds. The worst-case state of affairs could be that the borrower receives their refund and is taken into account ineligible for the utmost forgiveness due to their low mortgage steadiness on the time of announcement. However the borrower may merely take their refunded cash after which pay it proper again to their loans.

In fact, some debtors might choose to attend for extra concrete steering earlier than taking motion to keep away from doubtlessly losing their time. This might be significantly true for debtors who’ve a special mortgage servicer now than they did once they made their post-freeze mortgage funds, as it could be unclear which servicer is answerable for processing the refund.

In different circumstances, a borrower might have multiple mortgage servicer to cope with. On this case, the present servicer is the corporate that ought to be referred to as to provoke the refund course of. And, given the quick timeline till forgiveness might begin being processed, a borrower who is for certain that they are going to ask for a refund ought to achieve this as quickly as potential.

Influence Of The Momentary Public Service Mortgage Forgiveness (PSLF) Waiver

When the Public Service Mortgage Forgiveness (PSLF) program was initially carried out, it was created to forgive a borrower’s whole remaining Federal pupil mortgage steadiness for individuals who have spent 10 years working in a nonprofit or authorities job whereas making pupil mortgage funds. Nonetheless, tons of of hundreds of certified debtors have been rejected on account of seemingly inconsequential oversights (e.g., being on the flawed compensation plan, having the flawed mortgage kind, or making a fee that was only a greenback quick), complicated PSLF necessities, and poor administration by service suppliers.

In response to those shortfalls, the U.S. Division of Training introduced a plan to overtake the PSLF program in October 2021, which supplied a waiver quickly increasing the varieties of loans and compensation plans eligible for forgiveness beneath PSLF, amongst different adjustments made. As a part of this Public Service Mortgage Forgiveness (PSLF) Waiver, the Biden administration introduced a 1-year window for Federal pupil mortgage debtors to use their compensation historical past towards the 10-year compensation interval required by PSLF, whether or not or not any of their previous funds have been made to a beforehand ineligible mortgage kind or by way of an ineligible compensation plan, or have been disqualified earlier on account of minor technicalities.

Particularly, the waiver permits debtors who labored for eligible employers (Federal, state, and native governments and nonprofit organizations) throughout their mortgage compensation intervals to get credit score for his or her months of compensation when:

- Their loans have been beforehand ineligible FFEL loans;

- They have been on an ineligible compensation plan (i.e., not a 10-year Commonplace compensation plan or an extended Revenue-Pushed Compensation (IDR) plan; and/or

- Their fee was late, quick, or a lump-sum quantity.

Moreover, the waiver permits debtors who’ve consolidated a number of loans with overlapping compensation histories (e.g., a consolidation of loans acquired for each undergraduate and graduate levels) to obtain credit score for the most important variety of qualifying funds of the loans that have been consolidated (although presumably solely funds going again to October 1, 2007, when the PSLF program started, can be thought-about when making this willpower).

Whereas the waiver is slated to run out on October 31, 2022, the Biden administration’s Pupil Mortgage Debt Reduction Plan will replace the PSLF program by completely implementing a few of the adjustments launched by the waiver (defined later). Notably, whereas the waiver has been open for 10 months, it has to this point led to $10 billion {dollars} of mortgage forgiveness for 175,000 public servants. The Nationwide Bureau of Financial Analysis estimates {that a} complete of three.5 million debtors may doubtlessly profit from the waiver and that a minimum of $100 billion might be forgiven by way of the waiver if each eligible borrower have been to finish the steps required. And with solely two months left earlier than the waiver expires, at which level most of the guidelines will revert to the earlier necessities, debtors should take steps instantly in the event that they need to profit from the waiver.

Along with making a few of these vital adjustments launched by the PSLF waiver everlasting, the Biden administration’s aid plan additionally consists of the designation of 4 PSLF “Days of Motion”, devoted to debtors in particular sectors (authorities staff on August 24, educators on August 31, healthcare professionals and first responders on September 7, and personal nonprofits on September 14), to boost consciousness and encourage eligible debtors to use for forgiveness earlier than the waiver’s October 31 due date.

Future Adjustments To PSLF Made By Debt Reduction Plan

The Pupil Mortgage Debt Reduction Plan additionally consists of proposed future-looking adjustments to the PSLF program, most of which might completely prolong a few of the provisions (although crucially, not all) included within the PSLF Waiver. The proposed adjustments embody counting late, partial, or lump-sum pupil mortgage funds to qualify for PSLF. Up to now, a fee that was someday late could be thought-about ineligible for PSLF. Equally, lump-sum funds have been beforehand solely counted for one month, even when the quantity paid was sufficient to cowl multiple month’s required fee. The proposal would enable lump-sum funds to rely for a number of months of qualifying credit score in the direction of PSLF.

The proposed adjustments would additionally credit score the borrower beneath particular circumstances when their mortgage is in deferment or forbearance. For instance, if loans are positioned into deferment whereas debtors are enrolled within the Peace Corps or AmeriCorps, or if they’re on Nationwide Guard Responsibility or lively army service, the months when the mortgage was in deferment would now rely in the direction of PSLF even when no funds have been made. Previous to the PSLF Waiver, these deferments wouldn’t rely as qualifying months in the direction of PSLF. This proposal seems to be to make that change everlasting.

Though these provisions could be made everlasting by the Biden administration’s debt aid proposal on a forward-looking foundation, it’s vital to notice that as a way to get credit score for previous funds beforehand thought-about ineligible – even for funds like late or partial funds that will be eligible going ahead – debtors should nonetheless apply for the PSLF Waiver previous to the October 31, 2022 deadline.

How Fee Refunds Made Throughout The Freeze Could Influence The PSLF Waiver

The coverage allowing debtors to request refunds of funds made after March 2020, when the mortgage fee freeze was carried out, has a doubtlessly main impression on those that can profit from the PSLF Waiver. Which implies that those that can now qualify for PSLF by way of the waiver can doubtlessly have mortgage balances they might have paid down through the mortgage freeze refunded to them, and forgiven by way of PSLF as a substitute!

Instance 4: Grant took out FFEL loans to pay for his undergraduate research and opted into the Revenue-Based mostly Compensation (IBR) plan when he graduated in 2010. He obtained a job working as a nurse in a public college and made constant mortgage funds for the ten years he believed he wanted to qualify for PSLF.

In January 2020, Grant utilized for PSLF solely to study that his FFEL loans disqualified him and that he had 0 funds that certified for PSLF. At that time, annoyed by this system, Grant determined he would improve his funds to pay his debt down as shortly as potential, making funds of $700/month each month starting in January 2020.

When the PSLF Waiver was introduced in October 2021, although, Grant realized it was designed exactly for him. First, he referred to as his mortgage servicer, FedLoan, and requested for a refund of the 20 (funds comprised of March 2020 to October 2021) × $700 (month-to-month fee quantity) = $14,000 he had paid for the reason that fee freeze started.

As soon as his refund was full, he then consolidated his FFEL loans right into a Direct Consolidation mortgage and licensed his employment. As a result of he now meets the necessities to completely qualify for PSLF, and had already made the required variety of qualifying funds, his remaining steadiness has been completely eradicated.

Although the PSLF Waiver would nonetheless have permitted Grant’s full steadiness to be forgiven, had he not requested a refund of the funds that he made after the CARES Act mortgage fee freeze was introduced, he would have been out that $14,000.

As the instance above illustrates, it may make sense for debtors beforehand on a path to paying their debt to $0, however who are actually eligible to pursue PSLF (due to the PSLF Waiver), to ask for a refund of any mortgage funds they might have made since March 2020 when the mortgage fee freeze was introduced.

Newly Proposed Revenue-Pushed Compensation (IDR) Plan

The Pupil Mortgage Debt Reduction Plan features a newly proposed Revenue-Pushed Compensation (IDR) plan, which might go into impact in July 2023. The (as-yet-to-be-officially-named) ‘New IDR’ plan could be considerably extra beneficiant than any of the opposite present IDR Plans.

Whereas many questions stay about who can be eligible for the brand new IDR plan and what its remaining phrases can be, probably the most important coverage adjustments, maybe as important because the precise $10,000–$20,000 of aid being supplied to so many debtors, is the curiosity subsidy that guarantees to cowl the borrower’s unpaid month-to-month curiosity.

Curiosity Subsidies For Loans Beneath The New IDR Compensation Plan Will Assist Debtors Keep away from Future Unfavorable Amortization

Beneath the present IDR plans, debtors face the detrimental phenomenon of destructive amortization. This occurs when accrued mortgage curiosity grows bigger than the borrower’s required fee every month, which leads to an rising mortgage steadiness even when the borrower makes their required funds. Nonetheless, the curiosity subsidy provision of the brand new IDR plan would doubtlessly preclude any danger of destructive amortization and curiosity capitalization.

In line with the White Home Reality sheet:

…the proposed rule would totally cowl the borrower’s unpaid month-to-month curiosity, in order that – not like with present income-driven compensation plans – a borrower’s mortgage steadiness won’t develop as long as they’re making their required month-to-month funds…

By totally protecting unpaid month-to-month curiosity, the brand new IDR compensation plan would take away many issues confronted by debtors that at the moment stem from curiosity capitalization. Presently, when a borrower strikes from one compensation plan to a different, enters or exits forbearance, or refinances to a personal pupil mortgage, their unpaid curiosity capitalizes, which may end up in the borrower owing curiosity on curiosity.

Instance 5: Samir works as a public defender and has an Adjusted Gross Revenue of $60,000. When he went to regulation college, he borrowed $100,000 of unsubsidized Federal pupil debt at a 6% rate of interest and opted into the REPAYE compensation plan.

Samir’s complete annual mortgage fee was calculated to be $3,960 (primarily based on his discretionary earnings). Nonetheless, the entire curiosity due on his mortgage was 6% × $100,000 = $6,000, which implies that Samir had a complete of $6,000 – $3,960 = $2,040 of unpaid curiosity within the first 12 months.

Although the REPAYE plan has probably the most beneficiant curiosity subsidies of the present IDR plans (offering a 50% curiosity subsidy), it nonetheless leaves 50% of the remaining curiosity unpaid. So whereas 50% of Samir’s $2,040 is sponsored, it brings his complete unpaid curiosity right down to $1,020.

Assuming no main life adjustments, Samir can be including roughly $1,020 of curiosity to his mortgage steadiness yearly. After 5 years, then, Samir could have paid roughly $3,960 (annual mortgage fee) × 5 = $19,800, however now owes $5,100 extra {dollars} than he owed when compensation began!

At this level, Samir unintentionally forgets to recertify his earnings on time, as is required yearly, inflicting Samir’s account to be routinely moved into a special, much less beneficiant compensation plan. That is simply fixable, so Samir calls his mortgage servicer to repair it. Per week later, he’s put again into the REPAYE plan, however this triggers his excellent mortgage curiosity to capitalize. Which implies that his new principal steadiness is $100,000 (authentic steadiness) + $5,100 (excellent curiosity capitalized) = $105,100.

In fact, with the next principal steadiness comes greater curiosity. Thus, Samir now accrues $105,000 × 6% = $6,300 of curiosity yearly, which implies that in 12 months 6, his complete curiosity could be $6,300 – $3,960 (complete mortgage fee) = $2,340. And with the 50% curiosity subsidy, his unpaid curiosity after 6 years of paying would now be $2,340 ÷ 2 = $1,170.

Lots of the issues that come up from unpaid curiosity are sometimes made worse when a borrower’s circumstances are even much less favorable than in Samir’s instance above (e.g., they’ve a much less beneficiant compensation plan, bigger mortgage balances, smaller incomes, and many others.). Unfavorable amortization is a standard phenomenon for a lot of debtors; a research by the Congressional Finances Workplace in 2020 discovered that, for debtors who enrolled in IDR plans in 2010, over 75% of the debtors owed extra in 2017 than that they had initially borrowed!

Whereas this can be a non-issue for these pursuing PSLF (as PSLF quantities should not thought-about taxable earnings), it’s a large drawback for individuals who should not enrolled in PSLF and are on monitor for mortgage forgiveness as, per present regulation, the quantities forgiven beneath IDR plans will once more be thought-about taxable earnings after 2025. And after 20–25 years of compensation, many debtors discover themselves owing taxes on a good larger amount of cash than they initially borrowed.

The curiosity subsidy supplied by the newly proposed IDR plan would get rid of the potential for destructive amortization. From a purely monetary lens, this might considerably decrease the entire compensation prices to debtors, each in mortgage compensation and potential tax triggered by eventual forgiveness.

From a psychological standpoint, debtors would now not see their balances balloon over time. Even when they’re on monitor for PSLF with an expectation that their complete mortgage steadiness can be forgiven, it’s nonetheless laborious for debtors to see their steadiness rising over time (regardless of funds being made on time each month) with out worrying that they’re on the flawed path.

From a profession standpoint, a minimum of for debtors pursuing PSLF, there could also be fewer limitations to altering jobs, as the methods to cut back funds are most useful when their job is eligible for PSLF. However with out the dangers of destructive amortization and curiosity capitalization, there could also be extra flexibility for debtors to alter jobs with greater pay, as a substitute of remaining in a job purely as a result of their pupil mortgage steadiness had elevated a lot to the extent that the price of switching right into a non-PSLF-eligible job could be too nice.

Different Provisions Of The New IDR Plan

Borrower Eligibility. It’s nonetheless unclear who can be eligible for the plan. With previous rollouts of IDR plans, eligible debtors have usually been restricted to these with loans after a sure date. For instance, the “New IBR” plan is barely obtainable to new pupil mortgage debtors after 7/1/2014. Whereas we don’t know for sure, it appears seemingly that the newly proposed IDR plan will solely be obtainable to more moderen debtors as a substitute of all pupil mortgage debtors. For advisors, this may imply conserving a watch out for future steering to find out which (if any) purchasers is perhaps eligible to change to the brand new IDR.

Mortgage Eligibility. It appears seemingly that solely Direct loans can be eligible, and never Mother or father Plus loans. However that is purely hypothesis.

Willpower of Month-to-month Fee Quantities. The newly proposed IDR plan is considerably extra beneficiant than different IDR plans, as debtors can be required to pay solely 5% of their discretionary earnings in the direction of undergraduate loans, and 10% in the direction of graduate loans. Against this, different IDR plans require funds of 10%, 15%, or 20% of discretionary earnings.

For these with each undergraduate and graduate debt, funds can be calculated on a weighted common. For instance, a borrower with $10,000 of undergraduate debt and $20,000 of graduate debt must pay 5%×($10,000 ÷ $30,000) + 10%×($20,000 ÷ $30,000) = 8.3% of discretionary earnings beneath this plan.

Nonetheless, this plan additionally generously adjustments the calculation of “discretionary earnings.” In all prior IDR plans, discretionary earnings was calculated as an individual’s complete Adjusted Gross Revenue much less 150% of their poverty line (as decided by their household measurement). Within the newly proposed IDR plan, nevertheless, the calculation considerably decreases an individual’s calculated discretionary earnings by rising the share of the poverty line to 225%. Thus, beneath the brand new IDR plan, discretionary earnings is set as follows:

New IDR Plan Discretionary Revenue = Adjusted Gross Revenue – 225% × poverty line

For instance, three totally different debtors would have their mortgage fee quantities calculated beneath totally different compensation plans as follows:

Forgiveness. This plan requires the complete steadiness to be discharged after 20 years of constructing month-to-month funds on time. For these whose authentic steadiness is $12,000 or much less, the complete steadiness can be discharged after solely 10 years. The forgiven quantities can be thought-about taxable earnings.

Submitting Standing. We don’t know whether or not married debtors will be capable to file taxes individually in order that the calculation of their month-to-month funds is predicated on just one partner’s earnings. Whereas this technique is allowed on most IDR plans, it’s not allowed on the REPAYE plan.

Fee Cap. We don’t but know if there can be a fee cap for the newly proposed IDR plan, or how this plan will work for married {couples} when each spouses carry Federal pupil mortgage debt. Presently, if each spouses are on an IDR plan, their required funds get prorated proportionally to every particular person’s portion of the steadiness. This might change into way more troublesome when the required fee quantity is totally different for graduate versus undergraduate debt.

Remaining Questions About The New IDR Plan

The proposed IDR plan leaves lots of at the moment unanswered questions. A abstract of these are:

- Who can be eligible for the plan?

- What mortgage sorts are eligible?

- Will any curiosity accrue whereas debtors are at school and never but in compensation standing?

- How will married {couples} with each people on IDR plans be dealt with?

- Can married {couples} file taxes individually in order that earnings from solely the borrowing partner is used to calculate month-to-month funds?

The administration can be publishing the newly proposed IDR plan within the Federal Register within the coming days, with the U.S. Division of Training hoping to finalize the rule by November 1, 2022. If finalized by then, it’s going to go into impact on July 1, 2023.

Revenue-Pushed Compensation (IDR) And Public Service Mortgage Forgiveness (PSLF) Account Changes

Along with the Pupil Mortgage Debt Reduction Plan introduced in late August 2022, a separate announcement was made in April 2022 by the U.S. Division of Training concerning the Revenue-Pushed Compensation (IDR) and Public Service Mortgage Forgiveness (PSLF) Program Account Adjustment. The proposed account changes are designed to deal with previous issues with student-loan servicers incorrectly accounting for month-to-month funds made by debtors, which might negatively impression progress in the direction of mortgage forgiveness by way of IDR plans and PSLF.

By way of the account adjustment adjustments, the U.S. Division of Training (ED) will conduct a one-time assessment of the previous fee historical past of each pupil mortgage borrower on an IDR fee plan. Per the announcement:

- As a part of this initiative, ED will conduct a one-time revision of IDR-qualifying funds for all William D. Ford Federal Direct Mortgage (Direct Mortgage) Program and federally managed Federal Household Training Mortgage (FFEL) Program loans.

- ED will conduct a one-time account adjustment to borrower accounts that may rely time towards IDR forgiveness, together with

- any months wherein you had time in a compensation standing, whatever the funds made, mortgage kind, or compensation plan;

- 12 or extra months of consecutive forbearance or 36 or extra months of cumulative forbearance towards IDR and PSLF forgiveness;

- months spent in deferment (except for in-school deferment) previous to 2013; and

- any time in compensation previous to consolidation on consolidated loans.

- Any borrower with loans which have gathered time in compensation of a minimum of 20 or 25 years will see automated forgiveness, even if you’re not at the moment on an IDR plan.

- In case you have commercially held FFEL loans, you possibly can solely profit from the IDR account adjustment when you consolidate earlier than we full implementation of those adjustments, which is estimated to be no prior to January 1, 2023.

- In case you have made qualifying funds that exceed forgiveness thresholds (20 or 25 years), you’ll obtain a refund on your overpayment.

Importantly, these changes can have a major and speedy impression on PSLF candidates, particularly for individuals who spent lengthy intervals of time with their loans in forbearance or deferment.

Instance 6: Janet graduated from her social work program in 2014 with $90,000 of Federal pupil mortgage debt. In the identical 12 months she graduated, she started working as a social employee on the Veterans Administration (VA).

Janet struggled to make funds through the first 48 months out of college and spent the majority of that point (43 months) along with her loans in forbearance. She solely made 5 funds on time in these 4 years.

In 2018, she obtained her funds sorted out and enrolled within the Revised Pay As You Earn (REPAYE) plan. Since then, she has earned a complete of fifty monthly-payment credit towards mortgage forgiveness by way of PSLF.

Beneath the phrases of their Revenue-Pushed Compensation And Public Service Mortgage Forgiveness Program Account Adjustment, the U.S. Division of Training is anticipated to credit score Janet with 43 further months of credit score in the direction of PSLF forgiveness that she was beforehand ineligible for on account of being in forbearance.

Janet must file her employment certification kind for the time she was in forbearance and, as soon as filed, the division ought to replace her data to offer her credit score.

This brings her PSLF qualifying funds towards forgiveness up from 50 to 93, which means Janet is now simply 27 months away from forgiveness.

Because the announcement was made in April, no additional FAQs have been launched, so precisely how this program can be carried out stays unclear. Nonetheless, the announcement notes that “ED will start work on implementing these adjustments instantly, however debtors won’t see the impact of their accounts till fall of 2022.” Which implies that debtors ought to be reviewing their pupil mortgage accounts this fall to make sure they’re correctly credited for any months that ought to be eligible beneath this one-time adjustment.

Motion Steps To Entry The PSLF Waiver And IDR Account Changes

Debtors who work in public service and have FFEL loans can profit from consolidating their loans as quickly as potential. It is usually vital to file employment certification varieties for any months they labored at a qualifying job beginning in October 2007. Along with being required for PSLF, the consolidation can also be essential to entry the $10-$20k forgiveness introduced on August 24, 2022. So, even when a borrower doesn’t finish out qualifying for PSLF, there is no such thing as a sensible draw back to consolidation proper now and two totally different monumental potential upsides.

Debtors who have been beforehand on the flawed compensation plan to be eligible for PSLF ought to file their employment certification varieties for all months they have been beforehand ineligible. They’ll then enroll in a PSLF-qualifying compensation plan for when funds restart in January 2023. Going ahead, the requirement will as soon as once more be that debtors should be on a qualifying compensation plan to be eligible for PSLF. Qualifying compensation plans embody any of the IDR Plans (Revenue Contingent Compensation, Revenue Based mostly Compensation, Pay As You Earn, or Revised Pay As You Earn), in addition to the 10-Yr Commonplace compensation plan.

One other main change to the scholar mortgage panorama is totally different mortgage servicers. Beforehand, FedLoan was the servicer answerable for each borrower enrolled in PSLF. Nonetheless, FedLoan can be exiting the scholar mortgage servicing enterprise by the top of 2022. All debtors who’re pursuing PSLF will now have their loans managed by a special pupil mortgage servicer, MOHELA. FedLoan has already begun to ship its pupil mortgage accounts to MOHELA and can proceed this switch within the coming months.

As soon as their loans have been transferred to MOHELA, debtors ought to affirm that their month-to-month fee counts are correct. As whereas the U.S. Division of Training does have data of historic funds, previous servicer transitions have led to errors and inaccuracies. Moreover, those that are eligible for added credit by way of IDR Account Changes ought to see an up to date rely of eligible funds as soon as the handbook assessment of accounts has been accomplished someday this fall.

What Can Monetary Advisors Do Proper Now To Assist Shoppers Eligible For Reduction Maximize Their Advantages?

For advisors who need to assist their purchasers with pupil loans, conducting an audit to determine all purchasers with excellent Federal pupil mortgage debt generally is a good solution to begin. The primary resolution concerning pupil mortgage planning sometimes entails figuring out if the borrower intends to pay their debt to $0 or is working in the direction of some kind of forgiveness, both by way of the 10-year PSLF plan or by way of a 20–25-year IDR plan. The following step could be to find out if purchasers are nonetheless on the identical compensation path because the one they have been on previous to the fee freeze and if their present plan remains to be applicable for them.

For instance, if a consumer works at a nonprofit and has FFEL loans, their prior technique might have been to pay the debt right down to $0. However, with the PSLF Waiver and the 34 months (i.e., from March 2020 to December 2022) of PSLF credit debtors are doubtlessly eligible for all through the fee freeze, PSLF could also be a much better choice now.

Conversely, some debtors might have been on a path to PSLF however are actually eligible to have both $10,000 or $20,000 of their mortgage steadiness canceled from the brand new Pupil Mortgage Debt Reduction Plan. Relying on the brand new mortgage steadiness after the cancelation, their complete payoff prices might be decrease in the event that they have been to simply pay their debt right down to $0 than they’re to get to their 120 required funds for PSLF.

Reacclimating Debtors To Re-Set up Well timed Mortgage Funds

The seemingly resumption of pupil Federal mortgage funds firstly of 2023 implies that one of many key conversations for advisors to have with purchasers entails creating a technique for when their funds (lastly) do resume once more.

The primary and most evident consideration is how resuming pupil mortgage funds will impression the borrower’s finances. Advisors will help purchasers decide how a lot they will anticipate their funds to be once they resume, and be certain that the consumer makes any changes to their spending wanted to maintain a sustainable cashflow when that point comes.

Notably, this may occasionally or might not contain the borrower’s funds returning to the identical quantity that they have been paying pre-pandemic. In line with the studentaid.gov web site:

When you’re on a conventional compensation plan, equivalent to a Commonplace, Graduated, or Prolonged Compensation Plan, then your mortgage servicer might recalculate your fee quantity when the fee pause ends. Your mortgage servicer would base your new fee quantity on:

- your present steadiness of principal and curiosity and

- your remaining compensation interval.

When you’re on an IDR plan, your fee quantity will return to what it was earlier than your funds have been paused (except you’ve recertified or switched plans for the reason that fee pause started).

In different phrases, funds for non-IDR plans is perhaps recalculated primarily based on the present mortgage steadiness and the remaining time left on the mortgage, whereas for these on IDR plans, the brand new fee would be the identical because the previous pre-pandemic fee – as long as the borrower hasn’t recertified their earnings since earlier than the fee freeze started.

And though the annual earnings recertification requirement may also start once more in 2023, the earliest that any borrower might want to recertify their earnings can be July 2023 (and a few received’t be required to take action till effectively into 2024!), so most IDR debtors’ funds will resume on the identical degree as they have been in March 2020.

Talking of earnings recertification, one other a part of the consumer dialog would possibly contain planning for when the consumer will recertify their earnings when the brand new necessities kick in. When funds resume in January 2023, many debtors on IDR plans can be making funds primarily based on their 2018 earnings, which was the final 12 months for which tax info would have been obtainable when the fee freeze started in March 2020. Since earnings recertification takes into consideration earnings from the borrower’s most up-to-date tax 12 months, debtors whose earnings elevated between 2018 and 2021 would seemingly be higher off delaying recertification for so long as potential to maximise the variety of funds on the decrease pre-pandemic degree earlier than recertification causes them to extend – although if for some cause there was a lower in earnings since 2018, it will conversely make sense to recertify earlier than resuming funds in January 2023.

Lastly, getting ready purchasers for the resumption of pupil mortgage funds would possibly require a refresher on how the loans are paid. Many pupil loans might have modified servicers for the reason that final time funds have been made (for instance, FedLoan has stopped servicing loans and has begun transferring loans to MOHELA and different service suppliers, and debtors initially serviced by Navient have been transferred to Aidvantage), so debtors first have to be sure about who they’re repaying by checking their studentaid.gov account earlier than they begin making funds. Additionally they would possibly must create new login accounts, replace or change checking account hyperlinks, and replace autopay options to make sure their funds are made on time once they’re due in January.

In fact, if the borrower’s mortgage steadiness is fully worn out by the forgiveness program, or if they’ve change into eligible for forgiveness by way of PSLF or IDR through the fee freeze interval, debt forgiveness might need no direct impression on their month-to-month finances since there can be no funds to resume – though different elements, just like the impact of mortgage forgiveness on the borrower’s credit score rating, might need an extra oblique impact. However for everybody else, a actuality examine on what life seems to be like with the return of pupil mortgage funds can be a useful solution to transition again into making funds in 2023.

Calendar Of 2022–2023 Pupil Mortgage Dates For Monetary Advisors

Beneath is a abstract of vital dates regarding pupil loans for advisors to pay attention to:

Although many Federal pupil mortgage debtors might have gotten used to the thought of not making funds for the reason that starting of the fee freeze in March 2020 – and lots has occurred since then, between the COVID pandemic and the rollercoaster of financial uncertainty that adopted, that has confirmed to be extra vital within the large image – their mortgage burdens haven’t gone wherever within the intervening months. And for a lot of, neither has the accompanying nagging feeling of getting debt, even when that debt was within the service of making alternatives for the borrower that might have by no means existed with out entry to greater training.

The Biden administration’s Pupil Mortgage Debt Reduction Plan, subsequently, has the facility to be life-changing for a lot of people by wiping away a major quantity (if not all) of the debt burden that, for a lot of debtors, has been hanging round in stasis for over two years (and for a lot of debtors, had existed for years, if not many years, earlier than that). For different debtors, it represents a possibility to start making long-awaited progress on that debt – both by way of decrease, restructured debt funds calculated by the brand new Revenue-Pushed Compensation (IDR) plan or, for these now eligible, by way of future debt aid supplied by the Public Service Mortgage Forgiveness (PSLF) program.

For monetary advisors, that is an unbelievable alternative to attach with purchasers on a subject of deep significance and to offer useful steering on one of the best path ahead. Although the proposed plan’s advantages won’t be equal throughout all debtors, it’s a uncommon coverage announcement that, for nearly everybody, is impartial at worst and extraordinarily constructive at finest. Advisors can take this opportunity to the touch base with purchasers and have a good time with them – after which get right down to planning!