{kind=link}

Do you perceive the various varieties of rates of interest and the way they work? You possibly can make certain that lenders, bank card issuers, banks, and different companies who cost or pay curiosity know precisely how rates of interest work. In the event you don’t, you’ll be at an obstacle any time you store for monetary merchandise or negotiate with service suppliers.

As a shopper, you are able to do your self a favor by studying extra about how rates of interest work for each debtors and savers. This text will clarify how several types of rates of interest work in a standard language. That ought to enable you construct the information you could make borrowing, saving, and funding selections that give you the results you want.

There are two essential varieties of rates of interest that have an effect on you as a shopper: the curiosity you pay once you borrow cash and the curiosity you earn once you save or make investments cash.

Curiosity Charges in Borrowing

Whenever you’re borrowing cash, the rate of interest is the value a lender prices on your use of their cash.

The rate of interest a lender cost is predicated on a number of components, similar to:

- What’s the prime rate of interest is

- The borrower’s credit standing

- The mortgage kind

- The lender’s notion of the danger they’re taking

Let’s break these components down a bit.

1. The Prime Fee

Lenders set their rates of interest based mostly on what’s referred to as the Federal Funds Fee. The Federal Reserve units this price. That is the speed that banks cost once they lend to different banks.

The prime rate of interest or prime price is the everyday rate of interest banks cost to the very best (least dangerous) debtors. Generally, these are company debtors, and few people will qualify. The prime price is normally round three % above the fed funds price. Every financial institution units its personal price. The quoted “prime price” is a mean of the prime charges that main banks cost at a given time. As of January 2023, the prime price is 7.5%.

The prime price is used as a foundation for calculating different varieties of rates of interest, which are sometimes expressed because the prime price plus a set share. For instance, a variable rate of interest often is the prime price plus 5% or 5% above the prime price throughout any given interval.

2. The Borrower’s {Qualifications}

Lenders and bank card issuers base their pursuits on the perceived threat posed by a borrower. The riskier the transaction, the upper the rate of interest shall be.

Your credit score rating is the principle instrument that debtors use to judge threat, and it has a direct influence on the rate of interest you’ll pay. That is true whether or not you employ mortgages, loans, bank cards, or different varieties of credit score. The higher your credit score rating, the higher probability you have got of paying decrease rates of interest on the cash you borrow.

For instance, “subprime” debtors (credit score scores from 501 to 600) paid an common rate of interest of 12.93% on automotive loans in Jan. 2023. Debtors with “tremendous prime prime” credit score scores (781 to 850) paid a mean of three.84%.

Lenders may even contemplate different components of their threat evaluation, together with your schooling, revenue, employment historical past, and debt-to-income ratio.

3. The Mortgage Sort

Lenders cost completely different rates of interest for several types of loans. Secured loans, like a mortgage or automotive mortgage, typically carry decrease charges than unsecured loans, like private loans or bank cards. That’s as a result of the lender can seize the collateral that secures the mortgage when you don’t pay. In case your mortgage is unsecured, the lender has fewer choices.

Completely different loans additionally carry completely different ranges of threat. Most debtors will prioritize mortgage or automotive funds over bank card funds, and unsecured loans that may be discharged in chapter carry extra threat than secured loans.

For instance, the typical mortgage rate of interest for a 60-month automotive mortgage in Jan. 2023 was 4.07%. The typical rate of interest on a brand new bank card was 19.07%.

Mortgage Curiosity Charges

Mortgage curiosity is a bit completely different from most different rates of interest. A mortgage is without doubt one of the solely loans that an strange borrower with good credit score can get at beneath the prime price. On Jan. 12, 2023, the prime price is 7.25% and the typical 30 yr mounted mortgage price is 6.25%.

This variance happens for 2 causes:

- Mortgages are long run loans, typically 30 years.

- Mortgages are normally bought in a secondary market, the place they compete with bonds for funding patrons.

Due to these components, mortgage charges are usually based mostly on bond charges and total market situations reasonably than the short-term prime price.

Fastened and Variable Curiosity Charges

Mortgage firms provide two varieties of rates of interest on loans: mounted charges and variable charges. A mounted rate of interest on mortgage ensures that you just’ll be charged the identical rate of interest all through the lifetime of the mortgage.

In the event you tackle a mortgage with a variable rate of interest, the share of curiosity you’re paying on the mortgage can (and doubtless will) fluctuate over time. The curiosity will normally be the prime price plus an outlined “unfold” above that price.

Many variable rate of interest loans provide preliminary rates of interest that you’ll pay for a set interval. This price is normally beneath the prevailing price for fixed-rate loans. Nonetheless, variable price loans don’t include the safety that mounted price loans do. Whenever you join a variable price mortgage, you’re taking of venture that the preliminary decrease price will lead to a lifetime of much less curiosity paid. If rates of interest go up, the variable rate of interest in your mortgage may go up as effectively.

Solely you’ll be able to resolve if this can be a gamble price taking. Take into account the time period of the mortgage: the longer the mortgage time period, the larger the potential for rate of interest fluctuations. Additionally, contemplate the phrases of the variable price. Most variable price loans specify the frequency with which your price can improve, a most quantity that it will probably improve at one time, and a most price. All of those components have an effect on your alternative.

Annual Proportion Charges (APR)

Whenever you borrow cash or set up a revolving credit score line, you may even see two figures cited: the rate of interest and the Annual Proportion Fee or APR. The APR shall be a bigger quantity.

The APR represents the entire price of the credit score you’re taking on, together with the curiosity and any charges or different prices. If the mortgage has no prices apart from curiosity, the rate of interest and APR would be the identical.

You may discover two lenders each providing a 5% rate of interest on a mortgage. Nonetheless, the APR (which have to be disclosed on mortgage papers) for the 2 loans is perhaps completely different because of charges and different prices concerned with the mortgage.

It’s essential to have a look at the APR earlier than you signal any mortgage papers. The APR can provide you a extra correct image of the entire price of the credit score you’re making use of for.

Curiosity Charges in Saving and Investing

Whenever you’re saving or investing your cash, the rate of interest is the cash that the financial institution, bond issuer, or account supplier pays you for using your cash.

In the event you use another person’s cash, you pay for using that cash. When another person makes use of your cash, they pay you for the fitting to make use of it.

Curiosity on Financial institution Accounts

This happens once you maintain cash in a financial savings account, cash market account, certificates of deposit, or different interest-bearing accounts. That cash doesn’t simply sit in a vault: the financial institution makes use of it. They lend it to different individuals and pay you a portion of their earnings as curiosity.

Banks cost the next rate of interest for cash they lend than the rates of interest they pay to deposit account holders. The distinction within the two rates of interest, referred to as the “unfold”, is the place the financial institution earns its income.

Let’s say a financial institution pays you 1% in your CD stability. On the identical time, it prices you 5% on your auto mortgage, which matches the greenback quantity of your CD. They’re making a 4% revenue.

Bond Curiosity

Whenever you put money into bonds, you’re lending cash to the bond issuer. The bond issuer pays you curiosity on the cash it has borrowed. Like mortgage rates of interest, bond rates of interest are larger when the borrower is perceived as a excessive threat.

The US authorities is taken into account a really low-risk borrower, and the 10-year treasury bond price (Jan. 12, 2023) is 3.54%. A ten-year bond issued by the Brazilian authorities carries a 12.43% rate of interest, which signifies the next stage of perceived threat.

The identical distinction applies to company bonds. Ranking providers consider an organization’s creditworthiness and assign the corporate a ranking from AAA all the way down to D. That ranking is basically the corporate’s credit score rating: extremely rated bonds pay decrease curiosity than low-rated “junk” bonds.

Bonds normally pay larger curiosity than financial institution accounts since you are lending the cash your self and the curiosity on the mortgage goes solely to you. When a financial institution lends the cash you have got on the deposit, you share the curiosity paid by the borrower, and the financial institution typically will get a much bigger lower.

Do not forget that inventory market investments and lots of different investments don’t pay curiosity in any respect. Precise or anticipated good points that come from appreciation in asset worth should not curiosity and shouldn’t be handled as curiosity.

Annual Proportion Yield

The time period APY (Annual Proportion Yield, typically referred to as AER or Annual Efficient Fee) is basically the identical idea as APR, besides utilized to financial savings and investments. The APY describes the precise yield of an funding or interest-bearing account after any charges are deducted. Simply because the APR is normally larger than the cited rate of interest, the APY is often decrease than the cited rate of interest.

Funding may provide a return of 5% yearly. Together with charges, the precise price of return (APY) is perhaps 4.875%.

It’s essential to ask for or have a look at a contract’s APY earlier than committing to an funding.

Easy Curiosity

Most installment loans cost what known as easy curiosity. Your curiosity cost for a given month is solely calculated out of your present mortgage stability.

The rate of interest on a set mortgage stays the identical. The stability that the speed is utilized to will change as you pay the mortgage off. Every time you make a cost, your mortgage stability goes down. Your curiosity cost every month is calculated on the idea of your present stability, so your month-to-month curiosity cost will go down as your stability will get smaller. This course of known as amortization.

👉 For Instance: In the event you take out a automotive mortgage for $15,000 at a easy 4% rate of interest for a two-year mortgage interval, your cost will stay at $651.37 over the lifetime of the mortgage.

Let’s calculate.

You possibly can (roughly) calculate your curiosity for that first yr by performing some basic math.

$15,000 x .04 / 12 = $50 in curiosity per thirty days

It’s essential to notice that you’ll solely pay $50 of curiosity the primary month you have got the mortgage. That curiosity quantity will go down every month as a result of your mortgage stability will go down every month.

Right here’s an amortization schedule on the fictional two-year mortgage that may present you what I imply.

| Fee Date | Fee | Principal | Curiosity | Complete Curiosity | Stability |

|---|---|---|---|---|---|

| Jan 2023 | $651.37 | $601.37 | $50 | $50 | $14,498.63 |

| Mar 2023 | $651.37 | $603.38 | $48 | $98 | $13,795.25 |

| Apr 2023 | $651.37 | $605.39 | $45.98 | $143.98 | $13,189.86 |

| Might 2023 | $651.37 | $607.41 | $43.97 | $187.95 | $12,582.45 |

| Jun 2023 | $651.37 | $609.43 | $41.94 | $229.89 | $11,973.02 |

| Jul 2023 | $651.37 | $611.46 | $39.91 | $269.80 | $11,361.55 |

| Aug 2023 | $651.37 | $613.50 | $37.87 | $307.67 | $10,748.05 |

| Sep 2023 | $651.37 | $615.55 | $35.83 | $343.50 | $10,132.51 |

| Oct 2023 | $651.37 | $617.60 | $33.78 | $377.27 | $9,514.91 |

| Nov 2023 | $651.37 | $619.66 | $31.72 | $408.99 | $8,895.25 |

| Dec 2023 | $651.37 | $621.72 | $29.65 | $438.64 | $8,273.53 |

| Jan 2024 | $651.37 | $623.80 | $27.58 | $466.22 | $7,649.73 |

| Feb 2024 | $651.37 | $625.87 | $25.50 | $491.72 | $7,023.86 |

| Mar 2024 | $651.37 | $627.96 | $23.41 | $515.13 | $6,395.89 |

| Apr 2024 | $651.37 | $630.05 | $21.32 | $536.45 | $5,765.84 |

| Might 2024 | $651.37 | $632.15 | $19.22 | $555.67 | $5,133.69 |

| Jun 2024 | $651.37 | $634.15 | $17.11 | $572.78 | $4,499.42 |

| Jul 2024 | $651.37 | $636.38 | $15.00 | $587.78 | $3,863.05 |

| Aug 2024 | $651.37 | $638.50 | $12.88 | $600.65 | $3,224.55 |

| Sep 2024 | $651.37 | $640.63 | $10.75 | $611.40 | $2,583.93 |

| Oct 2024 | $651.37 | $642.76 | $8.61 | $620.02 | $1,194.17 |

| Nov 2024 | $651.37 | $644.90 | $6.47 | $626.49 | $1,296.26 |

| Dec 2024 | $651.37 | $647.05 | $4.32 | $630.81 | $649.21 |

| Jan 2025 | $651.37 | $649.21 | $2.16 | $632.97 | $0.00 |

Discover that as funds are made every month, the sum of money going towards decreasing the precise (principal) stability of the mortgage will increase. Conversely, the quantity of curiosity you pay decreases.

You possibly can see the monetary outcomes of straightforward curiosity from the mortgage amortization desk above. Or there’s a system you should utilize to determine it out for your self:

P x I / 365 x N

P x I / 365 x N stands for: the principal stability on the mortgage instances the rate of interest, divided by the variety of days in a yr instances the variety of days between funds.

So, for the two-year time period auto mortgage instance above, you’ll be able to work out the primary month’s curiosity by calculating $15,000 x .04 ($600) / 365 (roughly $1.64) x 31 = $50.96.

If it had been a 30-day month, the curiosity you pay throughout that first month would solely be $49.32. And when you made your funds with much less or extra time between funds, the quantity of curiosity you paid every month would range as effectively.

Utilizing calculations like these on easy curiosity loans or compounding curiosity investments helps you higher decide what you’re truly paying (or incomes). You should utilize our easy curiosity calculator that will help you decide what curiosity on a given mortgage or deposit shall be.

Compound Curiosity

Compound curiosity is curiosity paid on curiosity. When an account carries compound curiosity, the curiosity quantity is added to the stability, and subsequent curiosity funds are calculated on each the stability and the cumulative curiosity added.

The curiosity is added to the stability at common intervals. Compounding intervals could also be every day, weekly, month-to-month, quarterly, yearly, or another interval mounted by the lender.

To calculate compound curiosity, you could know three issues:

- The principal quantity.

- The rate of interest.

- The compounding interval.

The upper the speed and the shorter the compounding interval, the quicker the curiosity will accumulate.

Compound curiosity can give you the results you want if it’s being paid to you, and it will probably work towards you when you’re paying it.

Incomes Compound Curiosity

Most interest-bearing accounts carry compound curiosity. That signifies that you’ll earn curiosity in your curiosity funds in addition to the stability. Let’s see how that may work.

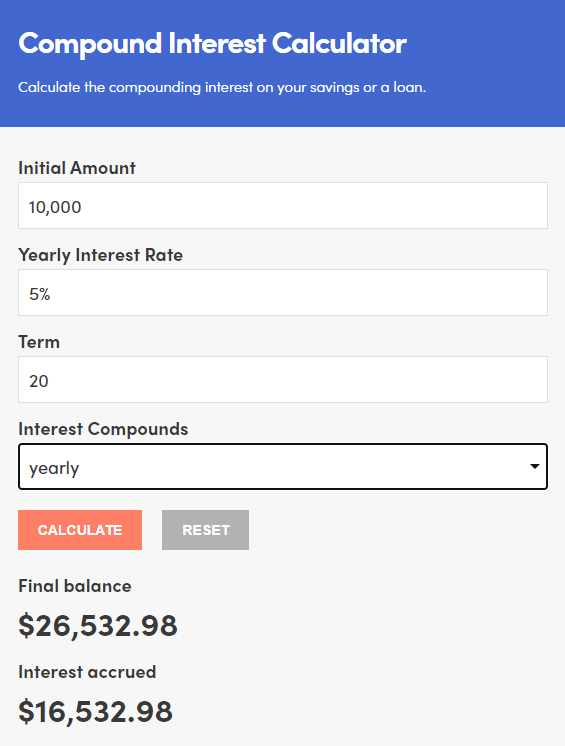

Let’s say you have got $10,000 in a set funding account incomes a 5% return, compounded yearly.

On the finish of yr one, you’ll have an account stability of $10,500. For yr two, you’ll now earn 5% on $10,500 as an alternative of merely your preliminary $10,000. This annual improve within the stability during which you earn curiosity will help your funding develop over time.

Right here’s what I imply.

In the event you had been to not earn compound curiosity in your $10,000 funding and easily earn your 5% for the subsequent twenty years, you’d have doubled your cash by the top of that point.

You’d have $20,000 after 20 years.

Nonetheless, when you think about compound curiosity the sum of money you’d have on the finish of 20 years adjustments dramatically. Let’s run these numbers by way of the FinMasters compound curiosity calculator and see what we get.

As you’ll be able to see, compound curiosity good points you a further $6,532.98.

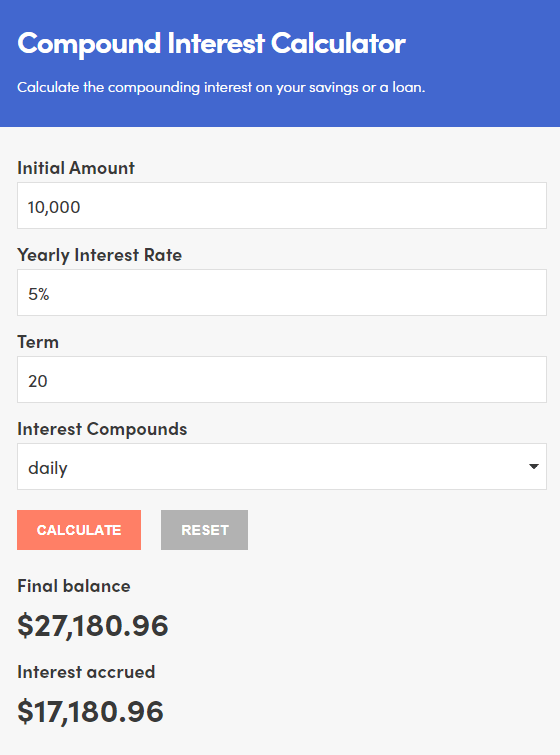

Now let’s have a look at what occurs if the curiosity is compounded every day.

The change in compounding interval earns you nearly $650 further.

The upper the speed and the extra frequent the compounding interval, the quicker compound curiosity will accumulate…

Paying Compound Curiosity, or Why Credit score Card Debt is So Harmful

Compound curiosity can give you the results you want when you’re incomes it, however it will probably work towards you when you’re paying it. This occurs most regularly with bank card debt. Bank card debt presents distinctive dangers, which come from the collision of 4 components.

- Low minimal funds. Many playing cards help you maintain your account in good standing with a comparatively accessible minimal month-to-month cost.

- Revolving credit score. Bank cards help you maintain spending. You possibly can add to your stability quicker than you pay it off, and lots of customers do.

- Excessive rates of interest. The typical US card price is 14.65%, and in case your credit score isn’t nice chances are you’ll be paying effectively over 20%

- Compound curiosity. Bank cards carry compound curiosity and the curiosity is normally compounded every day.

What does that imply in follow?

Let’s say you have got a $5000 stability on a card with a 15% rate of interest and a minimal cost of two%.

In the event you make solely the minimal cost every month, it should take you 27 years and 6 months to repay that stability, and you’ll pay a complete of $12,517.52… and that’s assuming you make no further purchases with the cardboard.

Many bank card customers have been caught in that entice, and realizing extra about find out how to repay bank card debt will help you keep away from being considered one of them.

Some monetary analysts describe incomes compound curiosity as “magic”. If that’s the case, paying compound curiosity – particularly with a excessive price and every day compounding – is perhaps referred to as black magic.

Abstract

Figuring out at the least somewhat bit concerning the several types of rates of interest is essential. That is true each for traders and debtors. On the naked minimal, it’s best to perceive the next phrases:

- Prime rate of interest – The speed provided to the very best (least dangerous) debtors.

- Compound curiosity – Curiosity that comes with earlier curiosity funds into the calculations.

- Easy curiosity – Curiosity that’s wholly based mostly on the unique sum invested or loaned.

- Annual share price – The rate of interest on a mortgage when charges are included.

- Annual share yield – The rate of interest on a financial savings account or different funding after accounting for charges.

- Fastened curiosity – An rate of interest that stays the identical at some point of a mortgage.

- Variable curiosity – An rate of interest that may (and doubtless will) fluctuate through the time it takes to repay a mortgage.

Figuring out these several types of rates of interest will make monetary planning simpler, whether or not you’re taking up debt, paying off debt, saving, or investing.