{kind=link}

That is for all you private-company workers on the market who nonetheless have your job. And have exercisable inventory choices hanging over your head, inflicting persistent low-key nervousness about:

Ought to I be doing one thing with these?

[Note: If you’ve been laid off, this blog post isn’t for you. You could check out our article about exercising ISOs or letting them turn into NSOs after you leave a company. You might instead, of course, be facing the decision of exercising your options or losing them entirely. That’s a stressful decision. Worthy of its own blog post. A blog post I haven’t written. Yet.]

Leaving your job forces your hand with regards to choices. There’s a 90-day deadline to do one thing.

In contrast, whilst you’re nonetheless employed, you don’t have to do something. You’ll be able to simply wait.

However perhaps that’s the improper method. What to do! Typically individuals are paralyzed with indecision. Typically folks mainly shut their eyes and leap into a giant resolution with out actually understanding the dangers and rewards of it.

We lately went by means of this train with a consumer at a big, pre-IPO, firm that’s doing fairly properly, even in these irritating instances.

The consumer has so many choices that exercising all of them could be actually costly. But additionally, they felt strain to perhaps do one thing? Isn’t that what you do with choices in personal corporations? It’s higher to train them as early as potential, proper?

Possibly. It actually all does rely deeply in your private monetary scenario and angle in the direction of threat. The “proper” reply after all additionally relies upon deeply on what finally ends up taking place with the corporate and its inventory…however you haven’t any management over or information of that future occasion. You’ll be able to solely know your individual private monetary and emotional scenario.

Excessive-Degree Framework for Making This Resolution

Making this resolution boils down to at least one factor, for my part: balancing the strain between these two needs:

- Minimizing how a lot cash you may lose

- Minimizing the tax price you pay on any beneficial properties

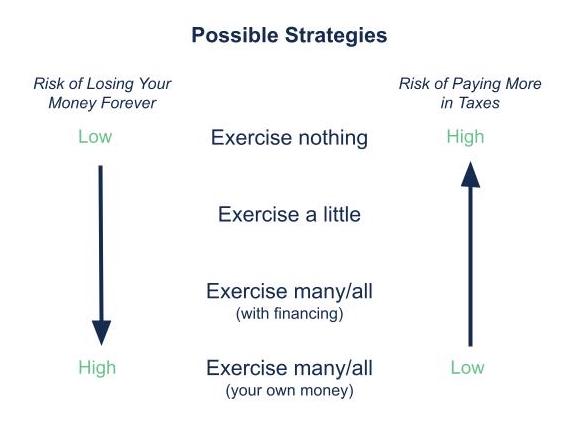

As I see it, you’ve 4 primary decisions with regards to choices at a non-public firm the place you may’t promote the inventory when you personal it:

- Train nothing and wait and hope for a liquidity occasion, earlier than your choices expire.

- Chip away very slowly by exercising as many choices as you may every year, with out incurring AMT (for ISOs) or incurring solely a small and acceptable quantity of tax (for NSOs). However largely you’re ready and hoping, as in above technique.

- Get financing to train (and pay taxes on) many/all exercisable choices now.

- Train many/all exercisable choices per yr, incurring/paying AMT

Remember that that is not an all-or-nothing resolution.

For the sake of brevity, I’m going to make use of the phrase “go public” all through this put up. What I actually imply is any liquidity occasion: going public, getting acquired, having a young provide…or one thing else I’m not considering of now.

Some Simplifying Assumptions I’m Making

I’m ignoring (the weblog put up can solely be so lengthy!) the potential for exercising choices and shopping for the shares after they qualify as Certified Small Enterprise Inventory. If you’ll be able to do that, then the long run capital beneficial properties tax price may very well be zero, which clearly could be very very good. If you happen to can purchase inventory out of your firm when it’s a Certified Small Enterprise, then that argues for exercising as a substitute of ready.

I’m assuming your choices value a significant amount of cash to train. In case your choices are tremendous low cost and there’d be no tax affect (which might be the case if the 409(a) worth of the inventory and your strike worth are the identical), then you may in all probability ignore all this neurotic considering under. You could possibly in all probability simply train all the choices now and put little or no of your cash in danger. This normally solely happens in very early stage corporations.

I’m ignoring the likelihood that the choices would possibly expire, which they’ll do both as a result of easy passage of time or since you’ve left the corporate.

Technique #1: Train nothing, wait, and hope for a liquidity occasion earlier than your choices expire.

Look, the rationale you train choices earlier than you have to (i.e., earlier than they expire, which might occur whenever you depart the corporate or simply for those who’ve caught round a actually very long time) is to get a decrease tax price on the hoped-for beneficial properties sooner or later.

So long as your choices aren’t expiring, I’m right here to say: You’ll be able to merely maintain them!

Professionals

You aren’t placing your individual cash in danger.

If your organization doesn’t go public, you’ll not lose any cash.

I’m telling you, as a monetary planner who’s seen lots of purchasers undergo personal corporations of various ranges of success, it is a Very Affordable Strategy.

Cons

If your organization ultimately IPOs like a nasty mamma jamma, and also you train and promote, you’ll find yourself paying the upper abnormal earnings tax or short-term capital acquire tax price (the charges are the identical, although the names of the taxes are completely different) on the beneficial properties as a substitute of the decrease long-term capital beneficial properties tax price.

This sounds scary to many individuals! And perhaps it is a giant distinction. Additionally perhaps it’s not as unhealthy as you worry. I encourage you to easily do some very primary, high-level arithmetic (not even “math”! Arithmetic) earlier than you begin knee-jerking “I don’t wanna pay increased taxes!”

Within the IPO yr, you’ll probably have an enormous earnings. So:

That’s 13.2% decrease.

If you happen to wait to train till you may promote your shares on the open market (i.e., your organization has gone public), you’ll pay 13.2% extra in taxes on the beneficial properties.

Possibly you assume that’s so much. Possibly that’s lower than you thought it could be. However not less than now you already know the distinction you’d truly cope with.

Technique #2: Chip away slowly and keep away from/decrease taxes.

You’ll be able to put “just a bit” cash in the direction of your choices every year. So little that you simply in all probability received’t even really feel it.

With ISOs, a affordable (if arbitrary) threshold is to train as many ISOs as you may with out incurring Different Minimal Tax (AMT). To determine this out, you may both:

- Work with a CPA (my favourite reply for just about all tax questions)

- Use Carta’s or SecFi’s exercising modeling instruments (for a much less strong however extra accessible instrument). Carta’s instrument is accessible solely to folks whose inventory plans are administered by Carta. SecFi is accessible totally free to everybody, although you do need to be keen to obtain advertising emails from them in alternate for entry.

With NSOs, you may select a small-ish (for you) amount of cash to decide to exercising the choices every year, as you will owe taxes on the train. The distinction between the strike worth and the 409(a) will depend as abnormal earnings, similar to your wage.

However largely you’re ready and hoping, as within the above technique, with the remainder of your choices.

Professionals

You might be placing minimal cash in danger.

If your organization doesn’t go public, you’ll not lose a lot cash. You won’t even really feel it.

If your organization does efficiently go public, then not less than you’ve some—albeit a small fraction of—shares that can get the decrease tax price.

Cons

If your organization goes public, you’ll pay a meaningfully increased tax price on many—not all—of your shares. Through which case, you’ll find yourself with much less cash after-tax than had you exercised your choices earlier.

Contemplate considering of this method as “the perfect of each worlds.” (The cynical amongst you can name it “the worst of each worlds.) A middle-of-the-road method. I love middle-of-the-road approaches with regards to issues of such profound unknowability. I feel it has the perfect likelihood of minimizing remorse.

Technique #3: Train (and pay taxes on) many/your whole choices now, utilizing financing.

By “financing,” I imply utilizing the providers of corporations like SecFi, ESO Fund, Vested, and EquityBee. These corporations will provide you with money proper now in alternate for a compensation later (when your organization goes public, sometimes) of that mortgage together with a portion of the shares you personal, if your organization inventory turns into worthwhile.

Sometimes these loans are “non-recourse,” which means that in the event that they mortgage you the cash, after which your organization goes <splat>, you don’t need to repay the mortgage.

Professionals

You aren’t placing your individual cash in danger.

So long as you train early sufficient, you’re going to get the decrease, long-term capital beneficial properties tax charges on any acquire in inventory worth between now and when you may promote your shares. If your organization goes public efficiently, you’ll save as much as the above-calculated 13.2% decrease tax price (by present tax brackets) in your beneficial properties.

If you happen to now personal the shares, meaning which you could ponder leaving your job (or be laid off) with out having to endure the added stress of “Ought to I fork over a ton of cash to train these choices inside the subsequent 90 days? Or lose them?” That is much less related if your organization’s inventory plan settlement says that your choices received’t expire after 90 days. Some more-“enlightened” corporations give inventory choices a 10-year expiration date, no matter whether or not you’re nonetheless on the firm.

And though I stated earlier that we’re assuming you’re not prone to your choices expiring, I’ll simply say right here that, by exercising now (which converts these choices to shares you personal), you now received’t lose choices on the expiration date. (This profit assumes your organization doesn’t have a “clawback” provision of their inventory plan settlement, which permits them to take again the shares, with fee, upon you leaving your organization.)

Cons

You hand over lots of your shares to the financing firm. The extra profitable the IPO is, the extra worthwhile these forfeited shares are, the extra painful it’s.

Relying on the type of financing, if your organization doesn’t efficiently go public and the inventory turns into nugatory/value much less, the mortgage may very well be forgiven.

Right here’s the kicker: that forgiven mortgage quantity could be thought of taxable abnormal earnings.

If the (forgiven) mortgage was for $500,000, then taxes may very well be roughly $190k (making a number of simplifying assumptions and utilizing this easy calculator). With no worthwhile firm inventory to pay it with. You’ve got an additional $190k mendacity round to pay in taxes, in alternate for inventory that’s value bupkus?

For my part, you must think about using financing primarily for those who’re leaving an organization (whether or not you need to or not), when it’s important to train now or lose the choices.

So long as you’re not prone to dropping choices, you actually don’t must sacrifice a giant proportion of the potential upside of your organization inventory to get financing. Taking the upper tax price hit (by ready) is probably going higher.

You actually simply have to check the numbers: if the financing firm desires 20% of your shares, however the additional tax could be “solely” 13.2%, then ready and paying the additional tax is healthier.

Until you’re dealing with dropping your choices, financing in all probability prices an excessive amount of.

Technique #4: Train (and pay taxes on) many/your whole choices now, with your individual cash.

That is the “most threat, most reward” technique. You train a bunch (perhaps even all) of your choices, utilizing your individual cash for each the strike worth and the probably hefty tax invoice.

Professionals

You get all the identical advantages as Technique #3 (financing) besides, after all, you’re placing your individual cash in danger.

Cons

You might be placing probably so much of your individual cash in danger. (“So much” is an idea relative to your psychology round cash and to the remainder of your funds.) If your organization doesn’t efficiently go public, you can lose as much as all of it.

Have you ever endangered your self by placing in danger extra money than you can safely lose? Are you able to not afford to fund necessary targets in your life (e.g., taking a sabbatical, going again to highschool, shopping for a house, charitable donations)?

Cash that you simply want for one thing necessary (both defending your self or giving your self actually necessary alternatives) is not cash you threat on this method.

If you happen to spend cash on personal firm choices, it’s important to assume you received’t see it once more and plan accordingly.

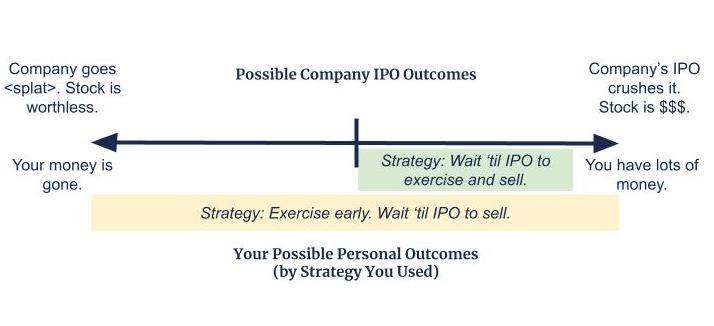

One other Perspective: The Resolution Has Uneven Dangers and Rewards

As I used to be scripting this weblog put up, I had a thought that was attention-grabbing sufficient (to me) to incorporate it, even when it doesn’t assist you to make your resolution. Possibly you’ll discover it thought-provoking, too!

Observe the asymmetry of threat and reward on this “Do I train or not?” resolution:

Let’s say you train none now and retain 100% of your choices, at no threat to your self.

- If your organization IPOs efficiently, you’ll profit 100% from that IPO. You’ll merely have a bigger tax chunk taken out of it.

- If your organization doesn’t IPO efficiently, you’ve misplaced no cash.

Your outcomes shall be “impartial” to “actually good.”

You’ve narrowed the spectrum of prospects to your cash scenario sooner or later. Sure, you’ve eradicated the perfect of the probabilities, however you’ve stored actually good ones and eradicated all of the unhealthy ones. By narrowing the probabilities, you’ve additionally made your future much less unsure.

Versus

Let’s say you train a bunch of choices now, placing a bunch of your cash in danger.

- If your organization IPOs efficiently, you’ll profit 100% from that IPO. Additionally, you will have a smaller tax bit taken out of it. Sure, you’ll find yourself with extra money than had you waited to train.

- If your organization doesn’t IPO efficiently, you’ve probably misplaced some huge cash. (Hopefully no more than you can “afford” to.)

- Whatever the final result, you’ve simply misplaced lots of liquidity. What? Meaning you’ve spent that cash now, so even when the IPO does occur efficiently…ultimately, till then, you haven’t any entry to the cash you place into the train.

Your final result may very well be anyplace from “Ohhhh, ouch, that’s unhealthy” to “Whoo, gonna purchase momma some new sneakers! After which a yacht!” The spectrum of prospects is huge, nearly unconstrained.

This can be a way more unstable, dangerous proposition.

For my part, the largest determinant of your wealth from firm inventory shouldn’t be going to be “did I train early or late?” It’s going to be if your organization went public or not, which is totally outdoors your management. Which may very well be a (maybe unusually) releasing realization!

Attempt to not overcomplicate the choice. Know that “luck” goes to be a method larger affect than anything. And, in that spirit, good luck.

Do you need to work with a monetary planner who might help you consider your largest monetary selections from the attitude of what has the perfect likelihood of funding a significant life? Attain out and schedule a free session or ship us an electronic mail.

Join Circulation’s twice-monthly weblog electronic mail to remain on prime of our weblog posts and movies.

Disclaimer: This text is offered for instructional, common data, and illustration functions solely. Nothing contained within the materials constitutes tax recommendation, a suggestion for buy or sale of any safety, or funding advisory providers. We encourage you to seek the advice of a monetary planner, accountant, and/or authorized counsel for recommendation particular to your scenario. Replica of this materials is prohibited with out written permission from Circulation Monetary Planning, LLC, and all rights are reserved. Learn the complete Disclaimer.