{kind=link}

Direct plan of a mutual fund affords higher returns than the common variant of the identical scheme. You already know this however how significantly better? Allow us to have a look at 10 years of reside knowledge and see the distinction. As we’ll see, even a small distinction in return compounds to a really large quantity because the time passes. We decide 6 in style MF schemes throughout classes for comparability.

The mutual fund corporations launched direct plans in January 2013.

Therefore, we have now over 10 years of efficiency historical past now. January 2013 – December 2022

Subsequently, it’s the proper time to match the efficiency between the direct and common plans of the MF schemes and the affect of decrease prices on portfolio values.

What are Common and Direct Mutual funds?

Every MF scheme has a direct and common plan variant.

Instance: Mirae Rising Bluechip-Common and Mirae Rising Bluechip-Direct.

Each the variants have the identical portfolio and the fund supervisor. Identical in all features. The one distinction is within the cost of commissions. Direct mutual funds don’t pay any commissions. Common (variant) of MF schemes pay commissions to distributors.

Due to commissions, common plan variant has a better expense ratio than the direct plan of the identical scheme. Decrease expense ratio in direct plans means decrease price.

And decrease prices in direct plans translate to raised returns than common plans.

We all know that the direct MF of X scheme will give higher returns than the common plan of the identical scheme.

Nevertheless, we can not straightforward admire how a small distinction in expense ratios (0.5% to 1%) can translate to a large variation in absolute returns.

Earlier, we needed to resort to assumptions to evaluate the affect. Nevertheless, now, we have now 9 years of knowledge.

Allow us to see the affect.

We are able to do a really complete train for this. Nevertheless, to drive house the purpose, I’ll decide up the preferred fund within the choose classes and present the affect.

- Nifty Index Fund –> UTI Nifty Index Fund

- Massive Cap –> Axis Bluechip Fund

- Multicap –> Mirae Rising Bluechip

- Mid Cap –> Kotak Rising Fairness Fund

- Small Cap –> SBI Small Cap

- Balanced Benefit Fund –> ICICI Prudential Balanced Benefit Fund

For energetic funds, I’ve merely picked one of many high three funds within the class (by measurement). My notion of recognition of a fund has influenced my alternative. And sure, the fund have to be round since Jan 2013.

Notice: This isn’t a suggestion to spend money on these funds.

You are able to do this train to your MF scheme and see the distinction.

Direct plan provides higher returns and this development will proceed

We are going to evaluate the efficiency on two features.

- Lumpsum of Rs 10 lacs invested on January 2, 2013

- SIP of Rs 10,000 per thirty days on the primary day of every month

To scale back the variety of charts, I’ll membership 2 funds in every chart. Don’t concentrate on the relative efficiency of those funds. Focus solely on the relative efficiency of normal and direct variants of every scheme.

UTI Nifty Index and Mirae Rising Bluechip

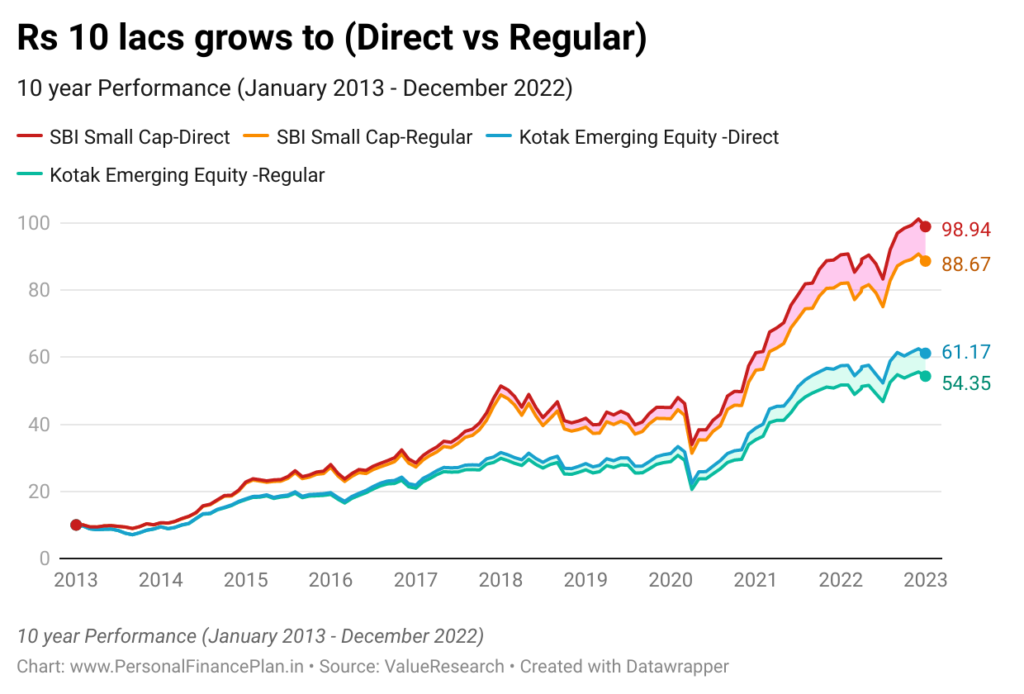

Kotak Rising Fairness and SBI Small Cap

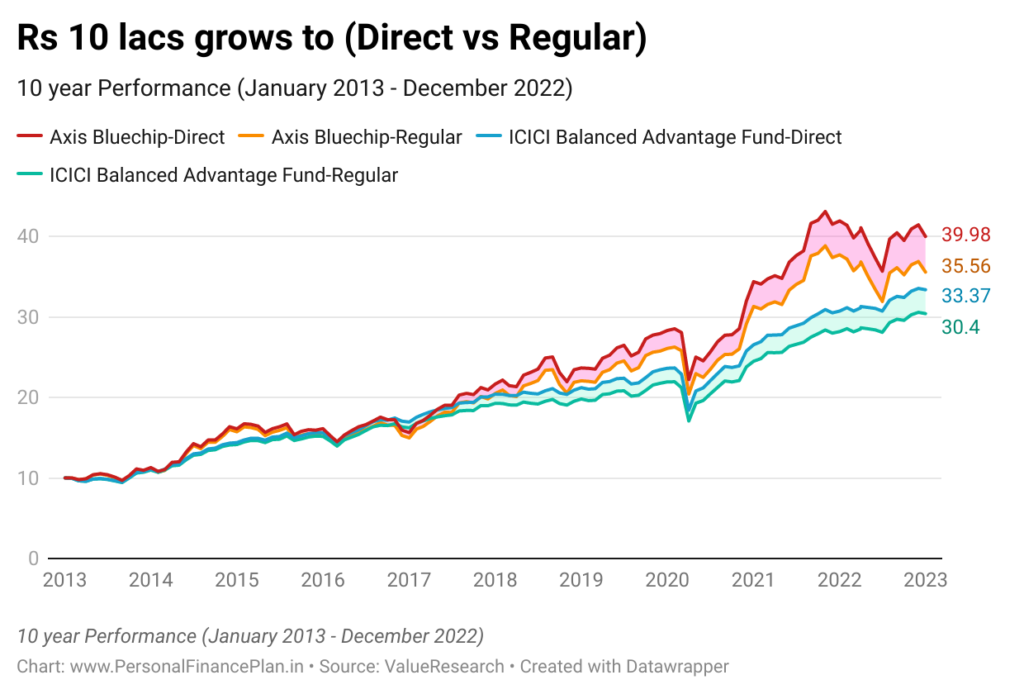

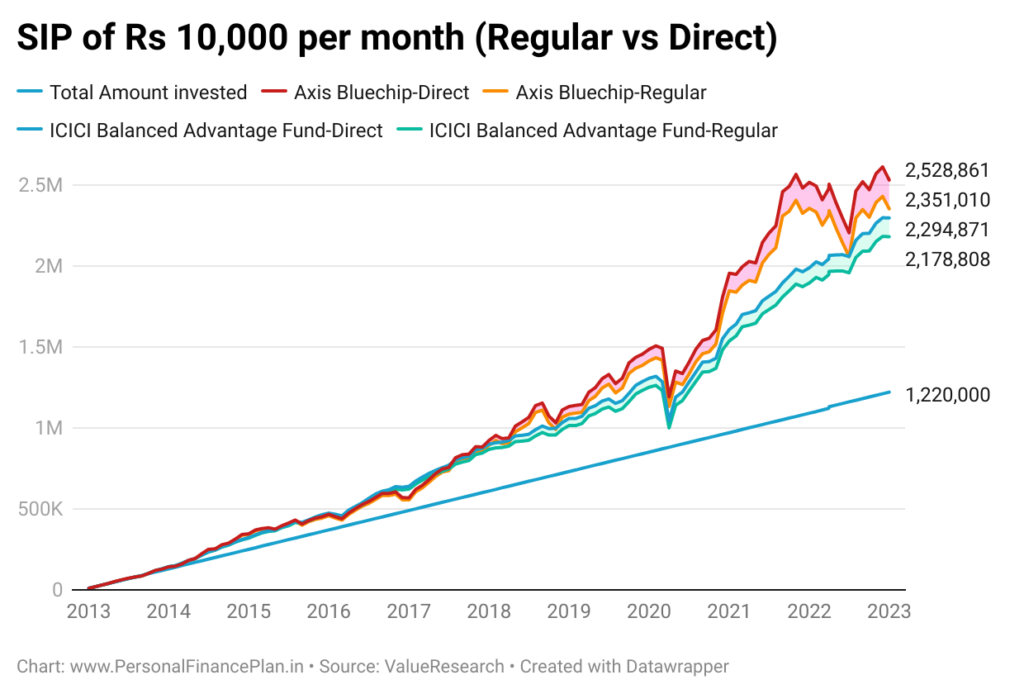

Axis BlueChip and ICICI Prudential Balanced Benefit

Simple to see you earn higher returns in direct plans.

Keep in mind, for every scheme, the direct and common variants began on the identical NAV in January 2013.

The NAV of the direct plan has grown quicker (than NAV of the common plan) since then.

Why?

No fee in direct plans –> Decrease Value –> Greater returns –> Quicker development in NAV

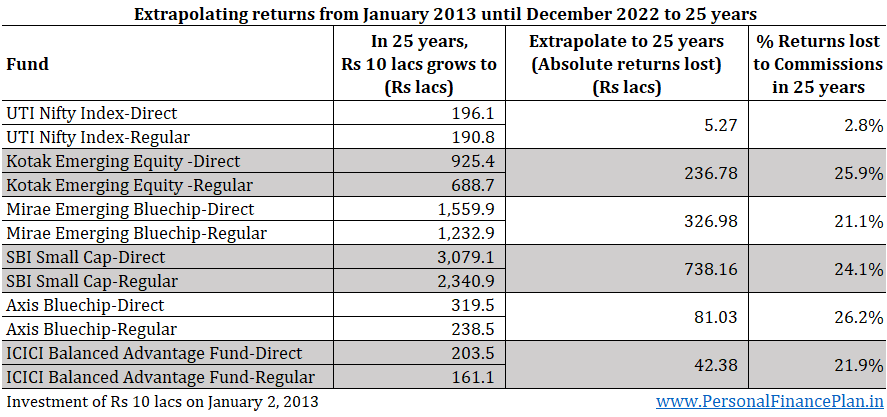

The portfolio (gross) returns are the identical for each common and direct plans. The direct plan inches forward due to decrease prices. The price distinction might look small (0.5-1.0%) but it surely makes substantial distinction over the long run. In all of the energetic funds shared above, you have got misplaced over 1/10th of the returns to distribution prices. That could be a large hit. And that is simply in 10 years.

Extrapolate this to 25 years (not proper however this may present the extent of returns forgone). If we had been to imagine that the funds had been to offer the same returns for a interval of 25 years, the commissions in common plans can eat nearly 1 / 4 of your returns.

The distinction between the NAVs of normal and direct plans will solely widen because the time passes. And it is a mathematical assemble. This hole between the NAV of the direct plan and the common plan will widen regardless of fund efficiency.

Confer with the chart beneath. On this chart, I present how the distinction between the portfolio worth (Rs 10 lacs invested on January 2, 2013) in direct and common plan has widened over the past 10 years.

The development is secular.

You will note a small dip (say March 2020) at a couple of locations within the chart. That’s simply the autumn in absolute distinction on account of market fall. Allow us to perceive with the assistance of an instance.

Allow us to say you invested Rs 1 lacs. The funding grows to 2 lacs in common plan and Rs 2.2 lacs in direct plan. The hole is Rs 20,000. Market corrects. Each fall ~10%. The portfolio will common plan falls to Rs 1.8 lacs. The portfolio in direct plan falls to Rs 1.98 lacs. The distinction falls from Rs 20,000 to Rs 18,000. Therefore the dips.

The distinction will proceed to extend.

A typical false impression is that the direct plans have greater NAVs. Therefore, you’ll get a lesser variety of models (than common plans). That’s proper however immaterial. What issues is which variant will give higher returns going ahead. And it is going to be the direct plan. I’ve addressed this query in this publish. The truth is, the NAV of the direct plan is greater than NAV of normal plan as a result of direct plan has given higher returns. Keep in mind, each the direct and common variants began on the identical NAV in January 2013.

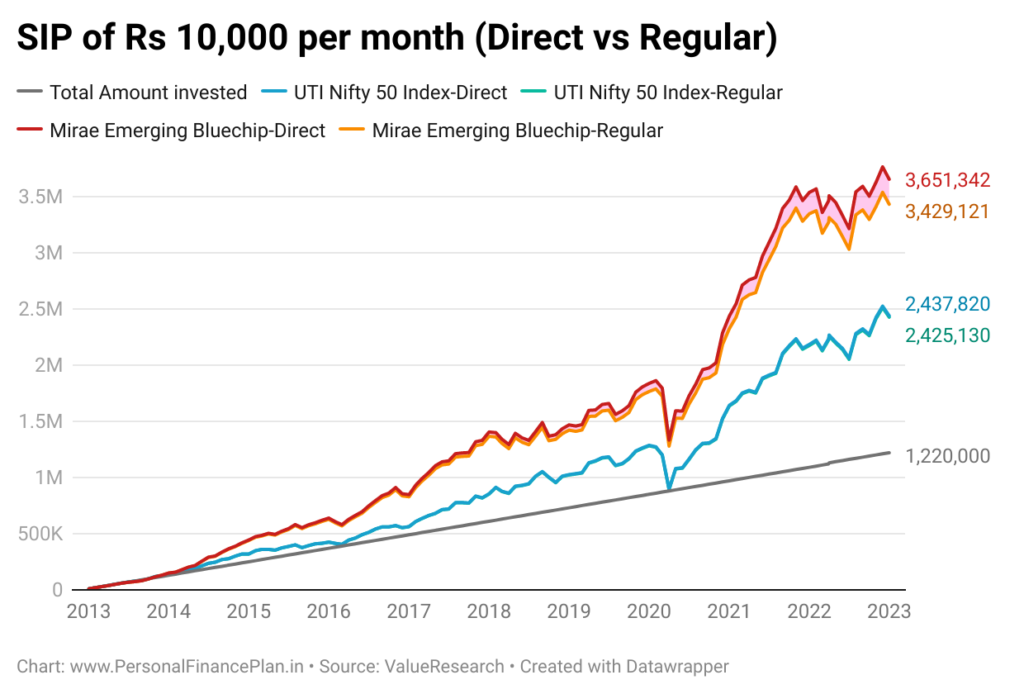

SIP doesn’t paint a distinct image

And there’s no cause it ought to paint a distinct image.

I plot the info for the SIP of Rs 10,000 on the first of every month since January 3, 2013, till March 31, 2022. 112 installments have gone in till now. Complete funding of Rs 11.2 lacs.

An fascinating level: The SIP began in Jan 2013. In early 2020, the portfolio worth in UTI Nifty Index goes down and touches within the quantity invested. So, 0% returns in over 7 years. SIPs don’t assure good returns.

No shock right here.

This distinction will proceed to develop.

The outcomes will range throughout schemes, fund class and AMCs. Debt MF schemes are more likely to pay decrease commissions in comparison with fairness funds. Throughout the fairness house, actively managed fairness funds pay greater commissions. Passive index funds pay decrease commissions. You possibly can test the distinction to your funds.

What do you have to do?

In case you are a Do-it-yourself investor, then it’s felony to spend money on common plans. You incur a further price for nothing. Now, it’s not a query of operational comfort both. The platforms akin to MFU, Kuvera, PayTM Cash, Zerodha Coin and Groww will let you spend money on direct mutual funds from a number of AMCs from a single interface.

In the event you search skilled help, you want to select.

You possibly can work with a distributor and spend money on common plans. You pay nothing to the distributor. The AMC pays the distributor in your behalf and adjusts the cost throughout the NAV. Subsequently, though you don’t write a cheque, you continue to pay for the recommendation and operational comfort. With common plans, there may be all the time potential for battle of curiosity. The middleman would possibly desire to push merchandise that supply greater commissions. As an example, since energetic funds will possible fetch higher commissions in comparison with passive funds, a distributor could also be extra inclined to recommend energetic funds. Your pursuits might take a backseat. Not essentially although. I’m certain there are numerous distributors who’re doing a superb job.

Notice (in case you are already working with a distributor): Regardless of my biases, I have to say common plans will not be evil. The MF distributors (who provide common plans) are offering a service and have to be compensated for it. In case you have been working with a trusted distributor who has helped construction your portfolio and delivered good returns, don’t grudge his/her compensation. Don’t simply evaluate the ten% you earned towards the 11% in direct plans. With out his/her steerage, your cash might have grown at solely 7% in financial institution FDs or at -5% in direct shares. Whereas the commissions will not be probably the most clear mode of compensation, admire the worth added. An advisor’s/distributor’s job is extra than simply choosing funding merchandise for you. On the identical time, be alert and conscious. Examine the expense ratios of beneficial MFs. Not good for you if the expense ratios are excessive. Push for low price merchandise.

Alternatively, you’ll be able to work with a SEBI registered funding advisor (RIA). Pay for the recommendation and spend money on direct plans. SEBI RIAs can have completely different work and compensation fashions. A hard and fast-fee mannequin, a share of asset based mostly or a mix of the 2. There isn’t any proper or fallacious mannequin. The compensation needs to be honest to each the investor and the adviser.

In case you are a brand new investor and simply desire a fast method to begin investments, attain out to advisers who work on 5-hour per consumer method. Their method will probably be cost-effective for you.

In case you are a critical investor and desire a custom-made resolution to your hard-earned cash and be extra concerned within the decision-making, you’ll be able to work with RIAs preferring a extra consultative course of and spend extra time with the buyers.